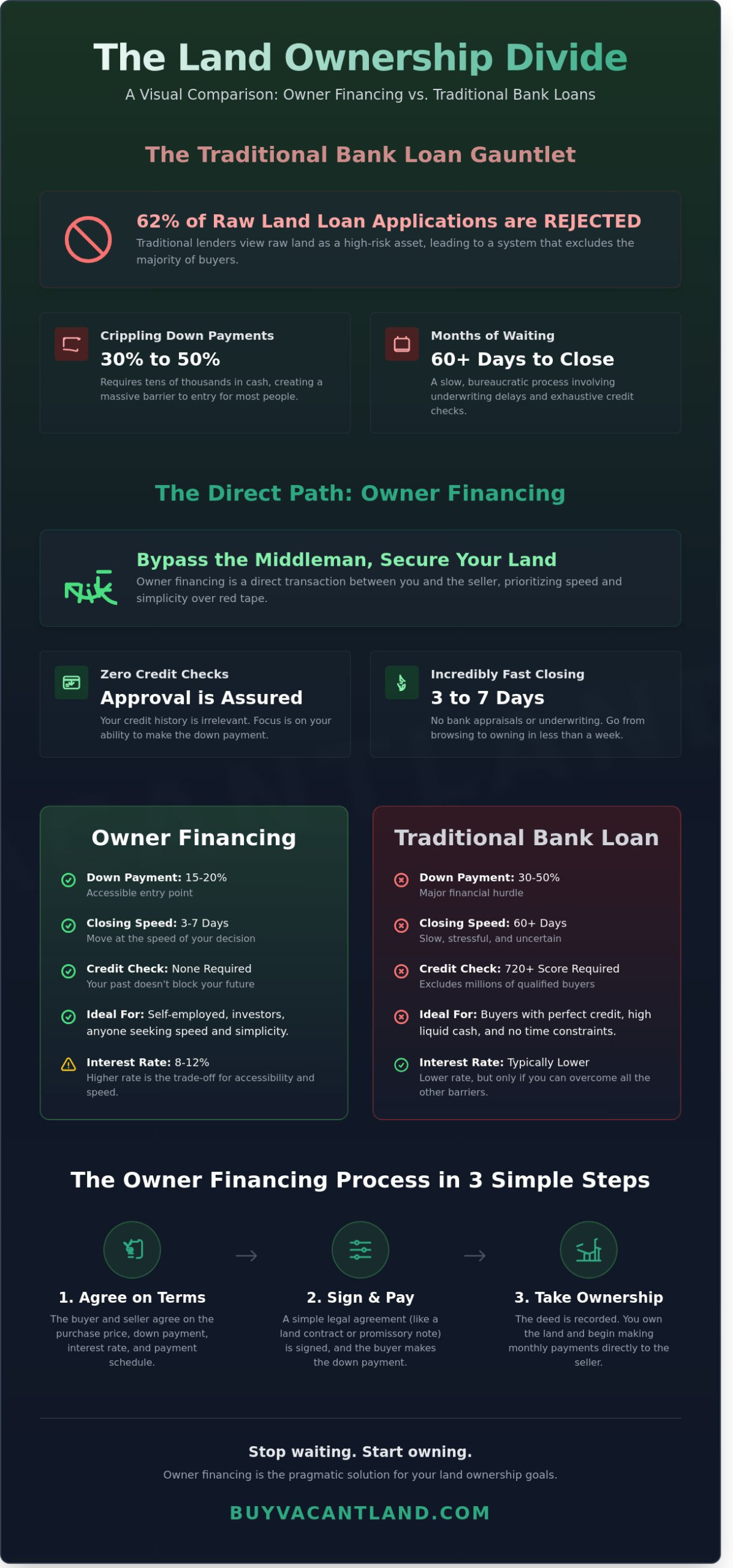

Stop letting a bank’s 720 credit score requirement stand between you and your property. Most traditional lenders reject 62% of raw land loan applications because they prioritize red tape over your goals. You’ve likely felt the frustration of high down payment demands and endless paperwork. It’s time to stop jumping through hoops for institutions that don’t value your time. Using owner financing land strategies allows you to bypass the middleman and secure your deed without the typical hurdles.

We agree that the current mortgage system is broken and unnecessarily slow. You deserve a simple path to ownership that doesn’t involve a credit interrogation or months of waiting. This guide promises to teach you how to secure land with zero credit checks and zero hidden fees. We’ll walk you through the entire legal process, provide a 5-point safety checklist for 2026, and give you direct access to active owner-financed listings. You’ll get the pragmatic facts you need to close your deal fast and start building your future today.

Key Takeaways

- Bypass bank red tape and secure property immediately using owner financing land with zero credit checks required.

- Understand the straightforward payment structure including down payments and flexible terms ranging from one to ten years.

- Compare the speed and accessibility of seller-direct deals against high-friction traditional bank loans.

- Execute critical due diligence steps to verify titles and ensure your new property is free of hidden liens.

- Skip the middlemen and browse thousands of direct listings on a specialized marketplace designed for speed and simplicity.

What is Owner Financing for Land?

Owner financing land is a direct transaction where the property seller acts as the bank. You don’t go to a traditional lender to secure a mortgage. Instead, you and the seller agree on a purchase price, a down payment, and a monthly installment plan. You make payments directly to the seller until the balance is paid in full. This arrangement bypasses the bureaucratic hurdles of big banks and puts control back into the hands of the buyer and seller. What is Owner Financing for Land? It is a streamlined path to property ownership that prioritizes speed and simplicity over paperwork.

This model exists because the traditional financial system is broken for land buyers. Most national banks view raw, undeveloped land as a high-risk asset. They worry that if a buyer stops paying, the bank is stuck with a piece of dirt that’s hard to liquidate. This fear leads to strict lending requirements that most average buyers can’t meet. Owner financing land solves this problem by removing the middleman. It provides immediate access to acreage with flexible terms and, in many cases, no credit checks at all. It’s a pragmatic solution for people who want to own land without the stress of a bank’s rejection letter.

This strategy is perfect for homesteaders, long-term investors, and anyone looking for a low entry cost. If you’re a self-employed worker or someone with a non-traditional income, you’ve likely felt the sting of a bank’s rigid debt-to-income requirements. Owner financing ignores those arbitrary hurdles. It focuses on your ability to make a down payment and your commitment to the monthly schedule. It’s about getting a fair cash offer or a manageable payment plan that fits your actual life, not a corporate spreadsheet.

The Problem with Traditional Land Loans

Banks make it nearly impossible to buy raw land with a small amount of cash. Most traditional lenders require a down payment between 30% and 50% for unimproved property. If you’re looking at a $40,000 parcel, you’ll need at least $12,000 to $20,000 in liquid cash just to get a seat at the table. This high barrier excludes millions of potential landowners who have steady income but haven’t saved five figures for a down payment.

The approval process is another major roadblock. A standard land loan often takes 60 days or longer to close. During this time, banks demand years of tax returns, pay stubs, and exhaustive credit histories. This rigid focus on debt-to-income ratios disqualifies the 15 million Americans currently working in the gig economy or running small businesses. You shouldn’t have to wait two months to find out if you’re “allowed” to buy a piece of property. The traditional system is slow, expensive, and outdated.

Why Sellers Offer Financing

Sellers choose this route because it’s efficient. By offering financing, a seller expands their pool of potential buyers by 400% or more. They aren’t limited to the small group of people who can pay all cash or qualify for a rare bank loan. This creates a faster exit for the seller and a better opportunity for you. It’s a win-win scenario that cuts through the red tape of the traditional market.

Sellers also benefit from a steady stream of passive interest income. Instead of taking a single lump sum and letting it sit in a low-interest savings account, they earn interest on the land contract. For the buyer, the most significant benefit is the timeline. You can often close a deal in as little as 3 to 7 days. There are no bank appraisals, no underwriting delays, and zero hidden fees. You get the land you want, and the seller gets a reliable payment stream. It’s the fastest way to turn a dream of land ownership into a recorded deed.

How Owner Financing Works: The Mechanics of the Deal

Owner financing land removes the middleman. You deal directly with the seller. The process begins with three specific numbers: the purchase price, the down payment, and the interest rate. Most sellers require a 15% to 20% down payment to secure the deal. You then make monthly payments over a fixed term, which typically ranges from 1 to 10 years. It’s a fast way to secure property without a credit check or a lengthy bank approval process.

Understanding How Owner Financing Works is essential for setting realistic expectations. While traditional mortgages might offer 30-year terms, land sellers prefer shorter timelines. Expect interest rates to sit between 8% and 12%. This rate is higher than bank rates because the seller is taking on the risk of the loan. However, the lack of red tape often justifies the cost for buyers who want to move quickly.

Most of these agreements include a “Balloon Payment” clause. You might make monthly payments based on a 20-year amortization schedule to keep the costs low. However, the loan term might only be 5 years. At the end of that 60-month period, the remaining balance is due in one lump sum. This structure works well if you plan to build a home and refinance with a construction loan or sell the property for a profit before the term ends.

Closing costs in these deals are significantly lower than traditional transactions. You avoid bank origination fees, expensive appraisals, and private mortgage insurance. Expect to pay between 2% and 5% in total closing fees. If you buy directly from a professional land company, there is often zero commission involved. This saves you thousands of dollars at the signing table. If you are looking to exit a property quickly, you can sell your land fast to a buyer who handles all the paperwork for you.

Note and Deed of Trust vs. Contract for Deed

In a Note and Deed of Trust, the buyer gets the legal title at closing. The seller holds a lien as security. This is the gold standard for buyer protection because it requires a formal foreclosure process if payments stop. A Contract for Deed, or Land Contract, is different. The seller keeps the legal title until you make the very last payment. This structure is simpler and faster to execute, but it offers fewer protections for the buyer’s equity during the payment term.

Key Terms You Must Negotiate

Negotiate your interest rate based on your down payment. If you offer 30% down, demand a rate closer to 7%. Ensure the contract has a 0% prepayment penalty. You should have the right to pay off the land early without extra fees. Finally, define the default grace period clearly. A 15-day window is a standard safety net. It prevents you from losing your investment over a simple technical delay or a late mail delivery.

Owner Financing vs. Traditional Bank Loans

Banks move at a glacial pace. A traditional land loan typically requires 45 to 60 days to close. You must endure appraisals, environmental surveys, and exhaustive background checks. Owner financing land cuts this timeline down to 72 hours or less. You skip the middleman and deal directly with the property owner. This speed is the primary reason savvy investors choose this route. You don’t wait for a loan committee to approve your dreams. You sign the papers and take possession immediately.

The cost structure differs significantly between these two paths. Banks offer lower interest rates, usually ranging from 6% to 8% for raw land. However, they bury you in upfront costs. You will pay a 3% origination fee, a $1,500 appraisal fee, and various processing charges. Owner financing often carries a higher interest rate, frequently between 10% and 14%. While you pay more interest over the life of the loan, you avoid the thousands of dollars in “junk fees” required at a bank closing. You keep your cash in your pocket for land improvements instead of giving it to a lender.

Accessibility is where the two methods diverge most sharply. Banks demand a credit score of at least 680 for land purchases. They also require a debt-to-income ratio below 43%. If you don’t meet these rigid metrics, they stop the process. Most owner-financed deals involve no credit check at all. Your ability to make the down payment serves as your collateral. This “No Credit Check” advantage opens the door for buyers who have been rejected by traditional institutions. It levels the playing field for everyone.

Flexibility of use is another critical factor. Banks often place restrictive covenants on what you can do with the property while they hold the lien. They might prohibit you from clearing timber, grading the road, or parking an RV on the site until the balance hits zero. Private sellers are far more pragmatic. They care about your monthly payment, not whether you are camping on the lot. Learning how owner financing works gives you the freedom to use your land your way from day one.

When a Bank Loan Makes Sense

Traditional financing is the right choice for high-value residential builds or massive commercial developments. If you’re planning a $750,000 construction project, a bank’s 5% interest rate will save you a fortune over 30 years. Banks also prefer land that already has a primary residence attached. If there’s a house on the property, you can often secure a standard 30-year fixed mortgage. This is only viable if your credit score sits comfortably above 800 and you have a 20% cash down payment ready.

Why Owner Financing Wins for Raw Land

Undeveloped land is “raw” and “unrestricted,” which makes it a nightmare for traditional underwriters. Banks see an empty lot as a high-risk asset. They often demand a 50% down payment to hedge their bets. With owner financing land, the barrier to entry is almost non-existent. Some parcels are available for as little as $250 down. You get your land today and start building tomorrow. You avoid the red tape, the 40-page applications, and the constant phone calls from loan officers. It is the fastest path to property ownership in the current market.

Due Diligence: How to Safely Buy Owner-Financed Land

Don’t buy land based on a promise. Protect your investment by verifying every detail before you sign. When you choose owner financing land, you skip the bank, but you shouldn’t skip the research. Start at the county assessor’s office. Verify that the seller’s name matches the deed exactly. A title company provides a professional title search for roughly $250 to $500. This small fee prevents a $30,000 mistake. If the seller isn’t the owner of record, stop the transaction immediately.

Check for hidden debts. Property tax liens or unpaid utility assessments follow the land, not the person. If the seller owes $4,200 in back taxes, you become responsible for that debt the moment the deed transfers. Demand a “clear title” as a non-negotiable condition of your purchase. You can check for these liens yourself at the county recorder’s office, or let a title company handle the paperwork for guaranteed accuracy.

Zoning determines your land’s actual value. Contact the county planning department. Ask specifically about “permitted uses” and “minimum square footage” for builds. Some parcels are zoned for agricultural use only. You might find you cannot build a home or even park an RV for more than 14 days. Never rely on a verbal agreement from a seller. A handshake deal is worthless in a court of law. Every term, payment date, and interest rate must exist in a written contract recorded with the county clerk.

The Essential Land Buyer Checklist

Verify these four items to ensure your land is functional and legal. Don’t assume the land is ready for use just because it looks empty. Check these specific points:

- Legal Road Access: Confirm the property has a deeded easement. Physical tire tracks don’t always mean you have the legal right to drive there.

- Utility Availability: Call the local power cooperative. Bringing electricity just 600 feet can cost over $12,000 in rural areas.

- Recent Survey: Ensure a licensed surveyor marked the boundaries within the last 24 months. Old stakes move or disappear.

- Closing Costs: Budget for recording fees and transfer taxes. Read more about Understanding Closing Costs for Land Sales to avoid financial surprises at the finish line.

Red Flags to Watch Out For

Watch for these three warning signs during your owner financing land transaction. First, avoid sellers who refuse to use a third-party escrow service for the down payment. Escrow protects your cash until both parties sign the contract. Second, walk away from “unrecorded” deeds. If the transaction isn’t filed with the county, you don’t legally own the property. This leaves you vulnerable if the seller tries to sell the same lot to someone else. Third, scrutinize the interest rates. While owner financing rates are naturally higher than bank loans, any rate above 15% is typically predatory. Most fair market deals sit between 9% and 12% in the current 2024 economy.

Find Your Next Property on BuyVacantLand.com

BuyVacantLand.com, operated by Buy Vacant Land Inc., serves as a specialized marketplace designed specifically for buyers and sellers of raw acreage. We connect you directly with property owners who offer owner financing land. This direct connection eliminates the need for traditional bank loans, credit checks, and the long wait times associated with institutional lending. You get direct access to the deed without the typical hurdles of a mortgage application. Our platform hosts listings across all 50 states, ranging from small 0.25-acre residential lots to expansive 100-acre ranch properties.

Traditional real estate transactions often involve heavy overhead. Standard agents frequently charge a 6% commission on the sale price. On a $40,000 land purchase, that equals $2,400 in fees that don’t add value to the dirt itself. Our marketplace removes these middlemen entirely. You deal with the seller. This structure allows you to negotiate terms that fit your specific financial situation. You can often secure a property with a down payment as low as $500, making land ownership accessible to those without massive cash reserves.

Finding the right deal requires the right tools. Our search interface includes a specific filter for “Owner Financing.” This tool allows you to bypass properties that require a full cash payment at closing. You can sort listings by monthly payment amounts and down payment requirements. This transparency ensures you only spend time looking at deals that fit your monthly budget. Once you find a parcel that meets your criteria, you can message the seller immediately through our secure portal. Ask them for a fair offer or request a customized payment schedule. Most sellers on our platform respond to inquiries within 24 hours, keeping your transaction moving at a fast pace.

Why Use a Specialized Land Marketplace?

Generic real estate websites like Zillow or Realtor.com focus primarily on single-family homes and urban condos. They often lack the specific data points land buyers need, such as soil quality, zoning classifications, or access to utilities. At Buy Vacant Land Inc., we focus exclusively on raw undeveloped land and “unrestricted lots.” This specialization streamlines your discovery of “cheap land for sale” by removing the noise of suburban housing markets. If you currently own property and want to move it quickly, you can List Your Vacant Land on Our Florida Marketplace to reach a dedicated audience of land seekers. We understand the nuances of rural parcels, ensuring you find the exact type of terrain you require.

Start Your Search Today

Buy Vacant Land Inc. has reduced the complex real estate process into three simple steps: Search, Connect, and Close. First, use our map-based search to identify owner financing land in your desired region. Second, use our internal messaging system to connect with the owner and finalize the terms. Third, sign the paperwork and close the deal. Many transactions on BuyVacantLand.com reach completion in fewer than 14 days. This speed provides a sense of relief and peace of mind that traditional 30-day or 60-day escrow periods cannot match. You get a guaranteed path to ownership without the stress of bank appraisals or surprises. Browse Owner Financed Land Listings Now and claim your piece of the American landscape today.

Take Control of Your Property Ownership Today

You don’t need a 750 credit score or a 20% down payment to own property in 2026. Traditional lenders often reject raw land applications, but owner financing land bypasses their red tape entirely. You work directly with the seller to set terms that fit your budget. This strategy eliminates the 60 day wait times common with bank appraisals and underwriting. Since 2016, BuyVacantLand.com has served as a specialized marketplace for these exact opportunities. We focus on 100% direct-to-seller listings that require 0 bank approval. Our platform simplifies the path to ownership into a few clear steps. You get a fast, guaranteed transaction without hidden fees or corporate delays. The market for vacant land is moving quickly, and waiting for a bank could cost you the perfect lot. Secure your future now by choosing a streamlined, no-nonsense approach to real estate. Your path to land ownership is ready when you are.

Find Your Dream Property with Owner Financing Today

You’ve got the tools to succeed, so go out and claim your piece of the map.

Frequently Asked Questions

Is owner financing land a good idea?

Owner financing land is a good idea if you want to bypass strict bank requirements. Traditional lenders typically demand a 35% down payment and a credit score above 700 for vacant lots. Seller financing allows you to secure property with 10% down and fewer hurdles. It saves you time and cuts out the middleman. You get the land faster while the seller earns interest. It’s a win-win for both parties involved.

Do I need a credit check for owner-financed land?

You don’t always need a credit check for this type of transaction. Many private sellers prioritize your down payment over a FICO score. While 20% of sellers might run a report, most rely on the land itself as collateral. If you stop paying, they take the land back. This makes it a fast solution for buyers with a 550 score or no history. You get the land without bank red tape.

What happens if I stop paying on a land contract?

You lose the property and all previous payments if you stop paying. Most land contracts include a 30-day default clause to protect the seller. If you miss the deadline, the seller starts a forfeiture process. You don’t get your down payment back. The seller keeps the land and any improvements you made. Read your 10-page contract carefully to understand these risks. It’s a serious commitment that requires steady payments.

Can I build on owner-financed land before it is paid off?

You can build on the land if your contract grants specific permission. Approximately 90% of sellers require written consent before you pour a foundation or install a septic system. You must also follow local zoning laws and building codes. If you default after building a $50,000 cabin, the seller keeps the cabin and the land. Get clear terms in writing to protect your investment. This ensures your construction plans are safe and authorized.

How much down payment is required for owner financing?

Expect to pay a down payment between 10% and 20% of the total price. On a $20,000 lot, you’ll need $2,000 to $4,000 upfront. This is significantly lower than the 40% often required by rural banks. Higher down payments can sometimes lower your interest rate by 2% or 3%. Negotiate your terms directly with the seller to find a number that works. It’s the fastest way to start your journey toward property ownership.

Who pays property taxes on owner-financed land?

The buyer is responsible for property taxes in most owner financing land agreements. You’ll either pay the county directly or include the tax amount in your monthly payment to the seller. Sellers often use an escrow service to manage these 12-month tax cycles. This ensures a 0% chance of a tax lien forming against the property while you’re still paying it off. Always confirm the tax status before signing your final paperwork.

Are there closing costs with seller financing?

You’ll face closing costs, but they’re minimal compared to bank loans. Expect to pay between $500 and $1,500 for document preparation and recording fees. This is a fraction of the 3% or 5% loan origination fees banks charge. You skip the $400 appraisal and the bank’s application fee. We focus on zero hidden fees to keep your transaction simple. You save money and close the deal in days, not months.

Is a land contract the same as owner financing?

A land contract is one specific method of owner financing. In a land contract, the seller keeps the legal title until you make the final payment. Other types, like a Deed of Trust, transfer the title to you immediately. Both options allow you to buy land without a bank. Choose the structure that fits your 5-year or 10-year financial plan. It’s a direct path to ownership that cuts through the usual corporate delays.

Join The Discussion