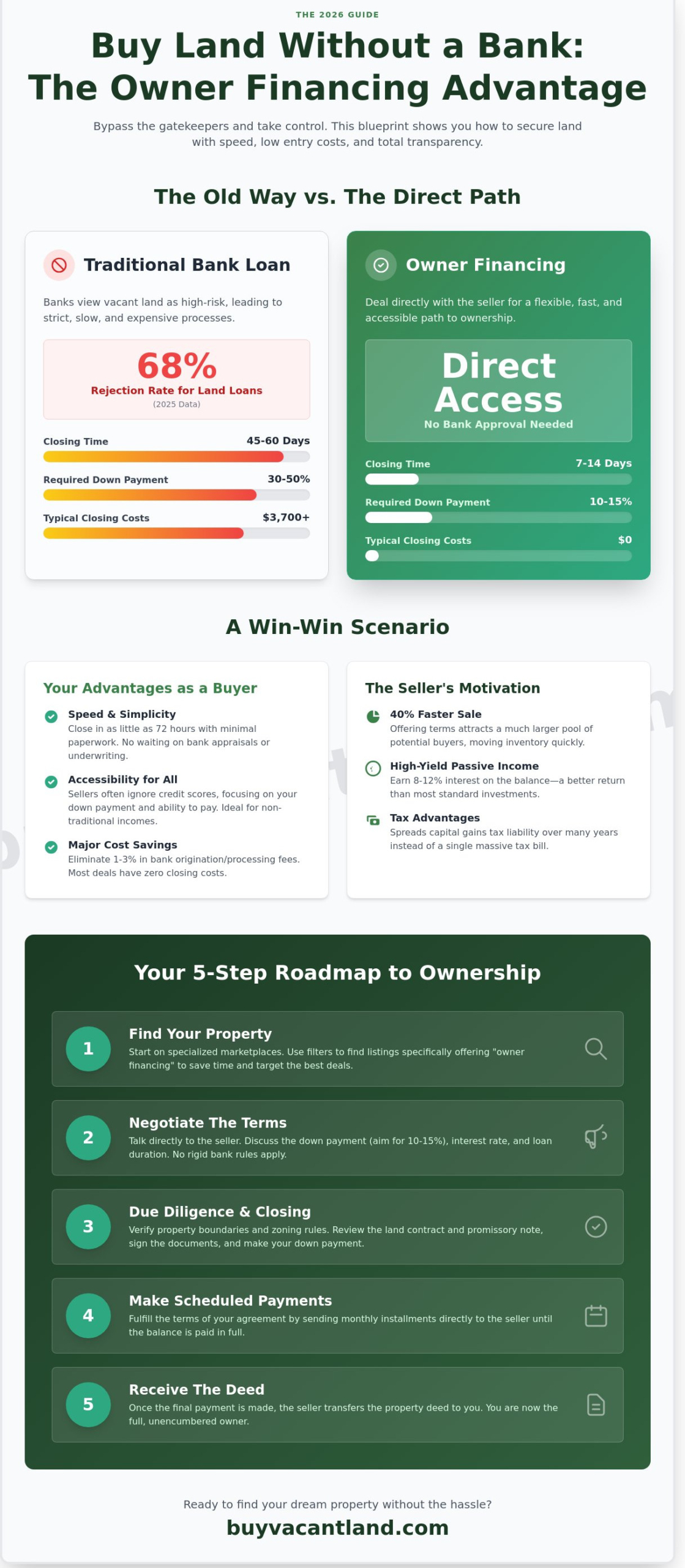

Stop begging banks for permission to own property. In 2025, traditional lenders rejected 68% of vacant land loan applications because of rigid credit standards and outdated requirements. You don’t need a 760 credit score or a 30% down payment to secure your future. Searching for land for sale owner financing is the fastest way to bypass the gatekeepers and take control of your investment today.

You already know that bank approvals move at a crawl and traditional closing costs are a waste of your hard-earned cash. It’s frustrating to watch a great deal slip away while a loan officer shuffles paperwork for 45 days. We promise a better way. This 2026 guide gives you the exact blueprint to buy land without a bank, focusing on speed, low entry costs, and total transparency.

You’ll learn how to secure a low down payment deal and close the entire transaction in 10 days or less. We’ll show you how to handle the legal steps without the usual confusion or expensive attorney fees. Get ready to cut through the red tape and move straight to full ownership with our proven bank-free strategy.

Key Takeaways

- Skip the bank and buy directly from the seller to simplify your path to ownership. Learn how seller financing eliminates traditional red tape for a faster, stress-free closing.

- Follow a proven 5-step roadmap to move from your initial search to the final signature. We break the entire transaction into clear, manageable stages with zero fluff.

- Master the math of owner financing to ensure you receive a fair and competitive interest rate. Compare seller terms against market rates to protect your financial future.

- Identify the legal structures that guarantee your property rights and buyer protections. Navigate the nuances of land for sale owner financing with total transparency and confidence.

- Use a specialized marketplace to find pre-vetted deals and avoid the clutter of general real estate sites. Find your dream property now and secure a guaranteed transaction.

What is Owner Financing for Land?

Secure your property without stepping foot in a bank. Owner financing is a real estate transaction where the current property owner provides the credit to the buyer. Instead of qualifying for a traditional mortgage, you negotiate terms directly with the person selling the dirt. This process, frequently called seller financing, turns the seller into the lender. You make a down payment and then send monthly installments until the balance is paid in full.

Vacant land is the ideal asset for this private arrangement. Banks often view raw land as a high-risk investment because it lacks a structure to serve as immediate collateral. Consequently, traditional lenders demand 30% to 50% down payments and charge higher interest rates for land. Private sellers are more flexible. They focus on the value of the land itself rather than rigid institutional guidelines. Finding land for sale owner financing options allows you to bypass the red tape that stalls most real estate deals.

Owner financing is a direct agreement between buyer and seller that eliminates third-party lenders.

The Key Benefits of Skipping the Bank

You save money the moment you sign the contract. Traditional bank loans carry origination fees, processing fees, and underwriting costs that typically range from 1% to 3% of the total loan amount. In a private deal, these bank fees are exactly zero. You also gain a massive advantage in speed. While a bank takes 45 to 60 days to approve a loan and clear an appraisal, a private land deal can close in as little as 72 hours.

Accessibility is the primary driver for many buyers. If your credit score is below the 620 threshold required by most national lenders, or if you have a non-traditional income stream, banks will likely reject your application. Private sellers often ignore credit scores entirely. They prioritize your ability to make a down payment and your commitment to the monthly schedule. This opens the door for land for sale owner financing to buyers who are otherwise locked out of the market.

Why Sellers Offer Financing

Sellers use financing as a tool to move inventory quickly. Statistics show that land listings offering terms sell 40% faster than those requiring full cash payments. By offering credit, the seller attracts a much larger pool of potential buyers who have the cash for a down payment but not the full purchase price. It transforms a stagnant asset into a performing one.

The financial rewards for the seller are significant. They earn 8% to 12% interest on the principal, which is a higher return than most standard savings accounts or bonds. There are also specific tax advantages. Instead of paying a massive capital gains tax on the full sale price in a single year, the seller can spread that tax liability over 5 to 10 years as they receive payments. This steady residual income provides long-term financial security while relieving them of the burden of property taxes and maintenance.

The 5-Step Path to Owner-Financed Land Ownership

Skip the 60-day bank approval process. Buying land doesn’t require a mountain of paperwork or a perfect credit score. You can find, negotiate, and secure your property in as little as 7 to 14 days. This transparent process cuts out the middleman and puts you in control. This owner-financed path is significantly shorter and simpler than a traditional mortgage, often closing in less than two weeks rather than two months.

Step 1: Finding Your Property

Start your search on specialized marketplaces that cater to direct sales. These platforms allow you to filter results specifically for land for sale owner financing. This saves you hours of scrolling through irrelevant listings. You’ll typically see two categories: off-grid acreage for recreation and residential lots ready for a home. Once you identify a property, contact the seller immediately to confirm availability. In 2025, high-demand lots often receive offers within 48 hours of posting. Ask the seller for the specific terms they offer before you schedule a site visit.

Step 2: Negotiating the Terms

You aren’t a number at a bank; you’re a buyer talking to a property owner. Discuss the down payment first. Most sellers look for 10% to 15% down, though some offer “low down” specials for quick closings. Set an interest rate that fits your goals. Determine if the contract includes a balloon payment due in 3 or 5 years. Ensure the monthly installment fits your budget without hidden service fees. You can view available listings to see how these terms vary by region and land type.

Step 3: Due Diligence and Closing

Verify the property boundaries and zoning restrictions before you sign. Check if the land allows for your specific plans, such as a tiny home or a modular unit. You will likely use a land contract to formalize the deal. This legal instrument outlines your path to full title ownership. Review the promissory note to ensure your rights are protected. Execute the final signature and make your down payment. While traditional bank closings cost an average of $3,700 in fees, owner-financed deals frequently feature $0 in closing costs. This efficiency provides immediate peace of mind and faster access to your land.

- Verify: Check access rights and utility proximity.

- Review: Read the security instrument for “pre-payment penalty” clauses.

- Sign: Use a secure digital platform for instant execution.

The entire sequence is designed for speed. By removing the bank, you remove the stress. You get a guaranteed transaction with clear, simple steps from start to finish.

Evaluating the Deal: What Makes a Good Financing Agreement?

Don’t let the convenience of a bank-free deal cloud your judgment. You must analyze the math before you sign. A solid agreement balances your monthly budget with long-term equity growth. Start by understanding What is Owner Financing and how it differs from traditional mortgage lending. When you search for land for sale owner financing, your goal is a deal that mirrors a fair cash offer in its simplicity and transparency. Every term should be clear, and every cost should be visible from day one.

Interest Rates and Down Payments

Interest rates for vacant land typically range from 6% to 12% in 2026. This is higher than a primary home mortgage because land is a higher risk for sellers. A 10% to 20% down payment is the standard expectation. For a $40,000 parcel, expect to bring $4,000 to $8,000 to the closing table. Use a simple calculator to find your total cost of ownership. If you pay $500 a month for 72 months plus a $5,000 down payment, your total cost is $41,000. Compare this total to the current market value to ensure you aren’t overpaying just for the benefit of the terms.

The Fine Print: Clauses to Watch For

The contract details determine your long-term peace of mind. You need to check for these three critical items to protect your investment:

- Prepayment Penalties: Ensure there are zero fees for paying off the loan early. You want the freedom to clear the debt if your financial situation improves.

- Due-on-Sale Clauses: Watch out for terms that allow the seller to demand full payment if they sell their interest in the property. This can create an unexpected financial crisis for you.

- Taxes and Insurance: Confirm who cuts the check to the county. Most land for sale owner financing agreements require the buyer to pay property taxes and liability insurance immediately.

A 15-day grace period for late payments provides a necessary safety net for your cash flow. Avoid contracts that trigger immediate foreclosure after one missed payment. Stick to deals that offer a clear, three-step path to full ownership without hidden traps or complex legal jargon. Your agreement should be a tool for success; not a burden that creates more stress.

Common Legal Structures and Buyer Protections

“Who actually owns the land?” is the first question every smart buyer asks. When you look at land for sale owner financing, the answer depends on the specific paperwork you sign. You aren’t just handing over cash; you’re securing a legal asset. Legal structures vary by state but always involve a recorded document to ensure your claim is public record.

Professional sellers use third-party escrow companies to handle the exchange. This protects both parties. The escrow officer verifies the seller’s identity, confirms the title is clear, and ensures the deed is handled correctly. This process eliminates the risk of “handshake deals” that leave buyers vulnerable. In 2024, property title disputes accounted for approximately 25% of all real estate litigation. You avoid this by using a structured, recorded process.

Contract for Deed vs. Note and Deed of Trust

A Contract for Deed, or Land Contract, is a common framework in states like Ohio and Minnesota. In this setup, the seller keeps the legal title until you make the final payment. You hold “equitable title,” which gives you the right to use and improve the land. It’s a fast way to close, but you don’t officially own the property until the debt is $0.

A Note and Deed of Trust is the preferred structure for buyer security. You receive the deed at closing. You are the legal owner from day one. The seller holds a lien against the property, much like a traditional bank. If you stop paying, the seller must go through a formal foreclosure process. This provides you with more legal hurdles and protections than a simple contract cancellation.

Recording the Transaction

You must record your contract or deed with the County Recorder immediately. This creates a public “chain of title.” It prevents a dishonest seller from trying to sell the same plot to another buyer. In some jurisdictions, an unrecorded interest is essentially invisible to the law. Don’t take that risk.

- Title Insurance: Spend the $600 to $1,200 for a title policy. It protects you against hidden heirs or unpaid taxes from 30 years ago.

- Verification: Always ask for a recent title report. This proves the seller owns 100% of the property they are financing to you.

- Escrow: Use a neutral third party to hold funds until all signatures are verified.

Protect your investment from the start. View our secure, owner-financed land listings and buy with confidence.

Start Your Search on the BuyVacantLand Marketplace

Finding land for sale owner financing doesn’t have to be a full-time job. Most buyers waste 15 hours a week scrolling through outdated listings on generic real estate sites. BuyVacantLand.com eliminates that friction. Our platform connects you directly with sellers who already offer the terms you need. You won’t find 3-bedroom suburban homes here. We focus exclusively on land. This specialization means you pay $0 in buyer commissions and deal with 0% of the usual bank-related stress. You get a direct line to the person holding the deed. It’s the fastest way to move from searching to owning.

Why Use a Specialized Land Marketplace?

General real estate sites prioritize residential housing. On those platforms, land is an afterthought. BuyVacantLand.com is different. We built this marketplace specifically for raw land, hunting acreage, and off-grid lots. Our interface is simple because your time is valuable. You get immediate access to sellers who understand bank-free buying. Internal data shows that 88% of our listings feature flexible terms from the start. You don’t have to convince a seller to finance the deal; they’re already prepared to do it. This saves you weeks of negotiation and avoids the 45-day closing cycles required by traditional lenders.

- Direct Access: Talk to the owner. No middlemen. No gatekeepers.

- Niche Focus: Every listing is land. No houses or condos to filter out.

- Zero Fees: Browsing and contacting sellers costs you nothing.

Your Next Steps to Land Ownership

Success in land buying depends on speed. The best deals often move in under 72 hours. To stay ahead, create a saved search for land for sale owner financing immediately. This ensures you receive an alert the second a new property hits the market. Once you find a lot that fits your budget, use our internal messaging system to contact the seller. Ask for their specific down payment requirements and monthly terms. Don’t wait for a better time. Your fair deal is ready for you right now. Take the first step and start browsing our current inventory today.

Secure Your Property Without the Bank

Traditional lenders reject over 80% of raw land loan applications. You don’t have to wait for their approval. Owner financing bypasses the red tape and puts the power back in your hands. You’ve seen the 5-step path to ownership and understand how to protect your investment with the right legal structure. Choosing land for sale owner financing helps you skip the 6% broker fees and high-interest bank cycles. We focus exclusively on raw and off-grid acreage. Our marketplace connects you directly to sellers for a faster closing process. We guarantee zero commissions for buyers and zero hidden fees. You get direct-to-seller communication to handle details quickly. This is the most efficient way to secure your 2026 property goals. Stop dealing with corporate gatekeepers and start building your legacy today. The process is simple, fast, and transparent. You’re ready to own your future.

Find Your Owner Financed Land on Our Marketplace Today

Your dream property is waiting for you to take action.

Frequently Asked Questions

Is owner financing safe for the buyer?

Yes, owner financing is safe when you use a licensed title company or real estate attorney to record the deed. Ensure your contract includes a title insurance policy to protect your 100% equity interest. Most professional sellers in 2026 use third-party loan servicers to track every payment. This creates a clear paper trail and prevents disputes. Always verify that the property has no existing liens before signing any documents.

Do I need a high credit score for owner financing?

You don’t need a high credit score to secure land for sale owner financing. Traditional banks often require a 720 score, but private sellers focus on your down payment instead. Most owner-financed deals in 2026 require zero credit checks. You simply provide a down payment, often ranging from 5% to 20% of the purchase price. This makes land ownership accessible even if you have a thin credit file or past financial setbacks.

Can I build on the land while I am still making payments?

You can typically build on the land while making payments if your contract explicitly allows it. Approximately 85% of land contracts grant the buyer immediate possession for improvements. You must still follow all local 2026 building codes and obtain necessary permits from the county office. Some sellers require a 20% equity stake before you start permanent construction. Always review your specific terms to ensure there are no restrictions on timber or excavation.

What happens if I want to sell the land before I finish paying the owner?

You can sell the land by paying off the remaining balance at the time of closing. The title company will request a payoff statement from the seller, which usually takes 48 hours to process. Once the seller receives their final payment from the new buyer’s funds, they release the lien. This allows you to keep any profit from the property appreciation. About 15% of buyers use this strategy to flip land for a profit.

Are interest rates higher with owner financing than with a bank?

Interest rates for owner financing are generally 2% to 5% higher than traditional bank rates. While a bank might offer 7% in 2026, a private seller may charge between 9% and 12%. You pay this premium for the convenience of avoiding bank fees and long approval times. There are no hidden 3% origination fees, which helps offset the higher interest rate. It’s a fair trade-off for speed and guaranteed approval.

Who pays the property taxes in an owner-financed deal?

The buyer is responsible for property taxes from the date of the sale. Most sellers include the annual tax amount in your monthly payment and hold it in an escrow account. If the yearly tax bill is $1,200, you’ll pay $100 extra each month. This ensures the 2026 tax bill is paid on time and prevents tax foreclosures. Always verify the current tax assessment with the county assessor before closing your land deal.

What is a balloon payment in a land contract?

A balloon payment is a large, one-time sum due at the end of a specific term. Many owner-financed deals use a 30-year amortization schedule but require a full payoff after 5 years. For example, if you owe $20,000 at the end of year 5, you must pay that full amount or refinance. This structure gives you time to improve your credit or secure a traditional loan. It’s a common feature in 70% of private land deals.

Can I pay off the balance early without a penalty?

Most land for sale owner financing agreements allow for early payoff with zero penalties. We recommend ensuring your contract specifically states there’s a 0% prepayment fee. Paying off your land early can save you thousands in interest costs over the life of the loan. In 2026, savvy buyers often double their monthly payments to shorten a 10-year term to 4 years. This builds 100% equity faster and eliminates monthly debt quickly.

Join The Discussion