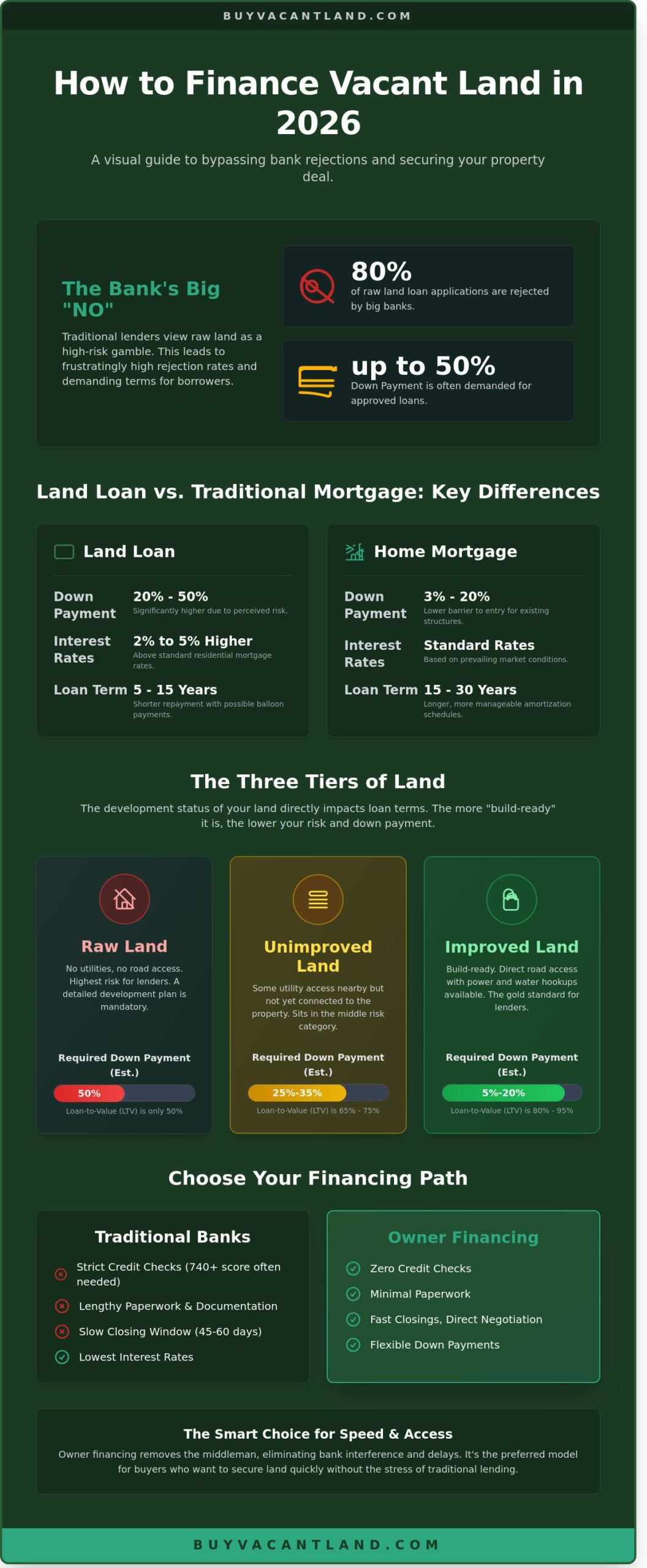

Most big banks reject 80% of raw land loan applications because they view vacant dirt as high risk. If they do say yes, they often demand a massive 50% down payment before you can even break ground. You’ve likely realized that learning how to finance a land purchase is far more difficult than getting a standard home mortgage. It’s frustrating to find the perfect parcel only to get stuck in a maze of confusing terms like unimproved versus improved property.

You deserve a clear path to ownership without the red tape. This guide provides a pragmatic roadmap to secure funding for your vacant land in 2026, regardless of your current cash on hand. We’ll show you how to skip the bank’s strict rules and find better alternatives. You’ll get a direct list of five reliable funding sources, specific steps to qualify for lower rates, and a proven strategy to find owner-financed deals that require zero bank intervention. It’s time to stop waiting and start building.

Key Takeaways

- Identify the crucial differences between land loans and mortgages to avoid common financing traps and bank rejections.

- Learn how the development “tier” of your land—Raw, Unimproved, or Improved—directly dictates your interest rate and down payment.

- Discover how to finance a land purchase using owner financing to bypass strict credit checks and traditional bank delays.

- Follow a simple five-step checklist to prepare your finances and target the right lender for your specific plot of dirt.

- Access a specialized marketplace where you can find guaranteed funding and listings with zero bank involvement.

What Is a Land Loan and Why Is It Different From a Mortgage?

Buying dirt requires a different playbook than buying a home. A land loan is a specialized financing tool used to purchase a plot of dirt with no existing structures. You can’t use a standard 30-year residential mortgage for this. Lenders treat vacant land as a completely different asset class because it lacks the immediate utility of a house. Learning how to finance a land purchase starts with accepting that the rules are stricter and the costs are higher.

Banks view land as a high-risk investment. If a borrower faces financial trouble, they’ll fight to keep the roof over their head. They’ll walk away from a vacant lot without hesitation. This reality makes banks nervous. To compensate for this risk, lenders impose tougher terms. You won’t find 3% down payments here. Expect higher interest rates, often 2% to 5% above standard residential rates, and shorter repayment terms. Most land loans require a full payoff within 5 to 15 years. A land loan is a high-equity credit facility for undeveloped property.

- Down Payments: These are your biggest hurdle. Expect to pay 20% for improved lots and up to 50% for raw, remote acreage.

- Interest Rates: Rates are higher because the secondary market for land loans is small.

- Repayment: You’ll likely face a “balloon” payment or a much shorter amortization schedule than a 30-year fixed loan.

The Core Difference: Collateral and Risk

A house is excellent collateral. It’s a finished product that a bank can sell quickly if you default. Raw land is different. A forest or a desert lot has no immediate “utility” for a lender. If they have to foreclose, they might sit on that property for years before finding a buyer. Big banks hate this lack of liquidity. They want to see you put significant skin in the game to ensure you don’t walk away when things get tough.

The 2026 Land Market Reality

The 2026 market shows a clear shift in how to finance a land purchase. Traditional bank liquidity for non-conforming land loans has tightened by 15% since 2024. Borrowers are moving away from local credit unions and toward private lending and marketplace-driven financing. These private options offer faster closings but demand higher interest. In 2026, speed is the new currency. If you want to secure a prime lot, you’ll likely need a private money partner or a significant cash reserve to bypass the red tape of traditional banking.

The Three Tiers of Land: How Your Dirt Affects Your Financing

Lenders don’t see all dirt the same way. The state of development dictates your loan terms. The closer a lot is to being build-ready, the lower your interest rate will be. Lenders categorize property into three distinct tiers: Raw, Unimproved, and Improved. Knowing these categories is vital when learning how to finance a land purchase without overpaying for your capital.

Raw Land: The Ultimate Challenge

Raw land is property with no electricity, no water source, and no paved road access. It represents the highest risk for a bank. Because there’s no collateral other than the dirt itself, a 50% down payment is the industry standard. You won’t get a loan without a detailed use plan. This document must show exactly how you’ll develop the parcel within a 12 to 24 month window. Banks want to see a clear path to a finished structure. If you find the financing hurdles for your current property too high, you can get a fair cash offer and walk away with liquidity instead.

Unimproved vs. Improved Lots

Unimproved land sits in the middle. It has some utility access nearby, but lacks a meter or a structure on-site. Improved land is the gold standard for lenders. It features direct road access, water hookups, and power at the curb. This type of lot functions most like a traditional home mortgage. When you understand how to finance a land purchase, you’ll see that “ready” land always wins the best terms. The Loan-to-Value (LTV) ratios typically break down as follows:

- Raw Land: 50% LTV (Requires 50% cash down).

- Unimproved Land: 65% to 75% LTV.

- Improved Land: 80% to 95% LTV.

Improved land is easier to secure because the infrastructure is already in place. This reduces the lender’s risk if you default. Banks can sell an improved lot much faster than a remote forest parcel. If you want a 2026 interest rate below 7%, target land that already has a power pole and a water tap.

Bank Loans vs. Owner Financing: A Pragmatic Comparison

Choosing the right path depends on your credit score and your timeline. Traditional banks offer the lowest interest rates. However, they demand the most paperwork. Most national lenders require a 30% to 50% down payment for raw land. They view vacant lots as high-risk assets. If you have a 740 credit score and a stack of tax returns, a bank is your cheapest option. If you want to move fast, the bank will slow you down. Expect a 45 to 60 day closing window with a traditional institution.

Hard money lenders sit on the other end of the spectrum. These are private investors who fund deals based on the land’s value rather than your income. Expect interest rates between 12% and 18% in the 2026 market. This is a short-term tool for investors who plan to flip the property or build quickly. It is not a sustainable way to hold land for the long haul. The high costs will erode your equity within months.

The Case for Owner Financing

Owner financing removes the middleman. You pay the seller directly in monthly installments. This is the fastest way to understand how to finance a land purchase without a bank’s interference. At BuyVacantLand.com, we prioritize this model because it works. It eliminates the stress of traditional lending. You get these specific benefits:

- Zero Credit Checks: Your past financial mistakes don’t stop your future ownership.

- Low Down Payments: Secure a 5-acre lot with as little as $1,000 down in many rural markets.

- No Red Tape: You can close the deal in 72 hours instead of 60 days.

Why Local Credit Unions Win Over Big Banks

National banks often ignore small land deals. Local credit unions are different. They understand the local soil. They know the value of a specific county’s growth. Data from 2024 indicates that credit unions approve land loans at a 15% higher rate than national giants. They offer the middle ground. You get better rates than hard money but more flexibility than a national bank. Use these steps to pitch your deal to a local officer:

- Bring a clear survey of the property.

- Show a simple plan for the land, such as clearing or fencing.

- Highlight your local ties to the community.

It’s a pragmatic choice for buyers who want a professional experience without the corporate headache. This strategy simplifies how to finance a land purchase while keeping your monthly costs manageable. Local lenders value the relationship over the algorithm. They see you as a neighbor, not a credit score.

5 Steps to Secure Your Land Financing

Securing a loan for acreage requires a specific strategy. Follow these five steps to understand how to finance a land purchase without the typical bank delays.

- Step 1: Optimize your financials. Clear immediate debt to lower your debt-to-income (DTI) ratio below 43 percent. Aim for a credit score of 680 or higher to unlock the best interest rates.

- Step 2: Identify your land tier. Lenders categorize property as Raw, Unimproved, or Improved. Your interest rate depends on which tier your land falls into.

- Step 3: Order a professional survey. Confirm all boundaries and legal access points before you submit your application.

- Step 4: Secure your down payment. Prepare to pay 20 to 35 percent upfront. This equity proves you’ve got skin in the game and reduces the lender’s risk.

- Step 5: Compare local lenders. Apply to three local credit unions or search for owner-financed listings to bypass traditional banking hurdles.

The Importance of the Land Survey

Lenders won’t touch a property without a clear boundary survey. An undisclosed easement or a zoning restriction can kill your financing mid-process. These legal hurdles represent too much risk for traditional institutions. A 2026 survey is the most critical document in your loan package. It ensures the land you’re buying matches the legal description on the deed and confirms you have legal physical access to the site.

Building Your “Land Package”

A professional land package speeds up the approval process. You’ll need tax maps, soil perc tests, and official zoning letters from the county. Provide a written plan for the property. A clear vision for farming, hunting, or building helps the appraiser determine the true value. For commercial deals, include a Phase 1 Environmental Site Assessment to confirm the land’s free of contaminants. This level of detail makes you a low-risk borrower. If you want to avoid the complexity of how to finance a land purchase, you can get a fair cash offer and skip the bank’s red tape entirely.

Skip the Bank: Find Owner-Financed Land on BuyVacantLand.com

Traditional banks often treat vacant land like a high-risk liability. They frequently demand 35% down payments and drag out the closing process for 60 days or more. BuyVacantLand.com eliminates this friction. Our specialized marketplace connects you with sellers who offer their own financing terms. This is the most efficient way to learn how to finance a land purchase without jumping through corporate hoops. You bypass the high-stress bank applications and deal directly with property owners who want to move land fast.

Speed is our priority. Most bank-financed deals fail during the appraisal or underwriting phase. On our platform, the seller acts as the bank. This means you can often secure a property in 10 days rather than 10 weeks. You get the land you want with simple, declarative terms that make sense for your budget. No red tape. No waiting games. Just straightforward land ownership that respects your timeline.

How to Use Our Marketplace Filter

Finding your next investment is simple and fast. We’ve stripped away the complexity to give you a clear path to ownership. Follow these steps to find the best deals:

- Step 1: Select your target state and county from our homepage.

- Step 2: Apply the “Owner Financed” filter to see instant terms and monthly payment options.

- Step 3: Sort by “Cheap Land” to find the lowest entry prices currently available in the 2026 market.

Buying direct saves you the standard 6% agent commission and thousands in hidden bank fees. We focus exclusively on vacant land. You won’t find distracting residential listings or commercial developments here. Our transparency ensures you see the total cost upfront. There are zero surprises and zero hidden charges. This marketplace is built for buyers who value their time and want to understand how to finance a land purchase with total clarity.

Conclusion: Taking Action Today

Financing is a hurdle, but it’s not a wall. You don’t need a 750 credit score to start your land portfolio. The 2026 land market moves fast, and waiting for a bank approval often means losing the deal to a cash buyer. Browse our current listings to see what financing is already available. Many sellers offer 0% interest or low monthly payments to get deals done today. Stop dreaming about property and start owning it. Start your land search on BuyVacantLand.com today and take control of your future.

Take Control of Your Land Investment

Learning how to finance a land purchase shouldn’t feel like a second job. You’ve seen the data for 2026. Traditional lenders still demand 35% down payments and months of paperwork for raw acreage. You don’t have to wait for a bank’s approval to start your project. Owner financing eliminates the red tape. It gives you a direct path to ownership with terms that fit your budget.

Success in real estate requires speed and clarity. You now understand the difference between improved lots and raw dirt. You know why direct seller agreements beat bank loans every time. At BuyVacantLand.com, we simplify the entire search. We provide direct access to land sellers nationwide. You pay 0 commissions. You deal with 0 hidden fees. We focus exclusively on undeveloped land to ensure you get the best possible value.

Your next property is waiting. Skip the middleman and secure your future today. Browse Owner-Financed Land Listings Now. You’ve got the tools and the knowledge. Now, it’s time to put your plan into action.

Frequently Asked Questions

Can I get a land loan with a 10% down payment?

You generally cannot get a land loan with only a 10% down payment. Most lenders in 2026 require a minimum of 20% for improved land and up to 50% for raw acreage. Local credit unions occasionally offer 15% down for specific build-ready lots. High risk levels for vacant property mean banks want more skin in the game. Plan for a 35% down payment to secure the best available terms.

How much are typical interest rates for land loans in 2026?

Typical interest rates for land loans in 2026 range from 7.5% to 9.5%. These rates sit 1.5% to 2.5% higher than standard 30-year residential mortgages. Commercial lenders might charge 10% or more for speculative purchases. Your credit score affects this heavily. A score above 740 secures the 7.5% floor, while lower scores push rates toward double digits quickly. It’s a simple trade-off for the bank’s increased risk.

Does the USDA offer loans for vacant land?

The USDA does not offer loans for standalone vacant land intended for long-term holding. They provide Section 523 and 524 loans specifically for site development if you build a home immediately. You must meet income limits, often capped at 115% of the median area income. These programs require a fixed construction timeline. You won’t get funding for “buy and hold” investment strategies through the USDA in any state.

What happens if I buy land and can’t get it financed?

If you fail to secure funding after signing a contract, you typically lose your earnest money deposit, which is usually 1% to 3% of the purchase price. You must include a financing contingency in your offer to avoid this. Without that clause, the seller can sue for specific performance. Knowing how to finance a land purchase before signing prevents this 100% loss of your deposit and keeps your cash safe.

Is owner financing safe for the buyer?

Owner financing is safe if you use a licensed title company and record the deed immediately. This method bypasses bank red tape and speeds up the process. Ensure the contract specifies that your payments go toward the principal. About 20% of private land sales use this method to avoid strict 2026 bank requirements. Always demand a title insurance policy to protect your investment from hidden liens or past ownership disputes.

How long does it take to close on a land loan vs. a home mortgage?

Land loans typically close in 21 to 30 days, while home mortgages often take 45 to 60 days. The process is faster because there’s no structure to inspect or appraise. You save roughly 3 weeks by skipping the traditional home appraisal and 10-day inspection period. This speed allows you to move from offer to ownership in less than a month if your paperwork is ready for the title company.

Do I need a land survey before applying for financing?

Most lenders require a professional land survey completed within the last 12 months before they approve financing. Surveys cost between $500 and $2,500 depending on the lot size and terrain. The bank needs to verify property boundaries and check for encroachments. Understanding these costs is vital when learning how to finance a land purchase effectively. Don’t rely on old markers or verbal promises from the seller.

Can I use a personal loan to buy a small lot of land?

You can use an unsecured personal loan for land purchases under $50,000 if your credit score is above 680. These loans offer fast cash but come with higher interest rates, often exceeding 12% in the current market. There’s no collateral, so the bank doesn’t place a lien on the land. This strategy works best for small recreational lots where traditional lenders refuse to provide small-dollar financing for vacant property.

Join The Discussion