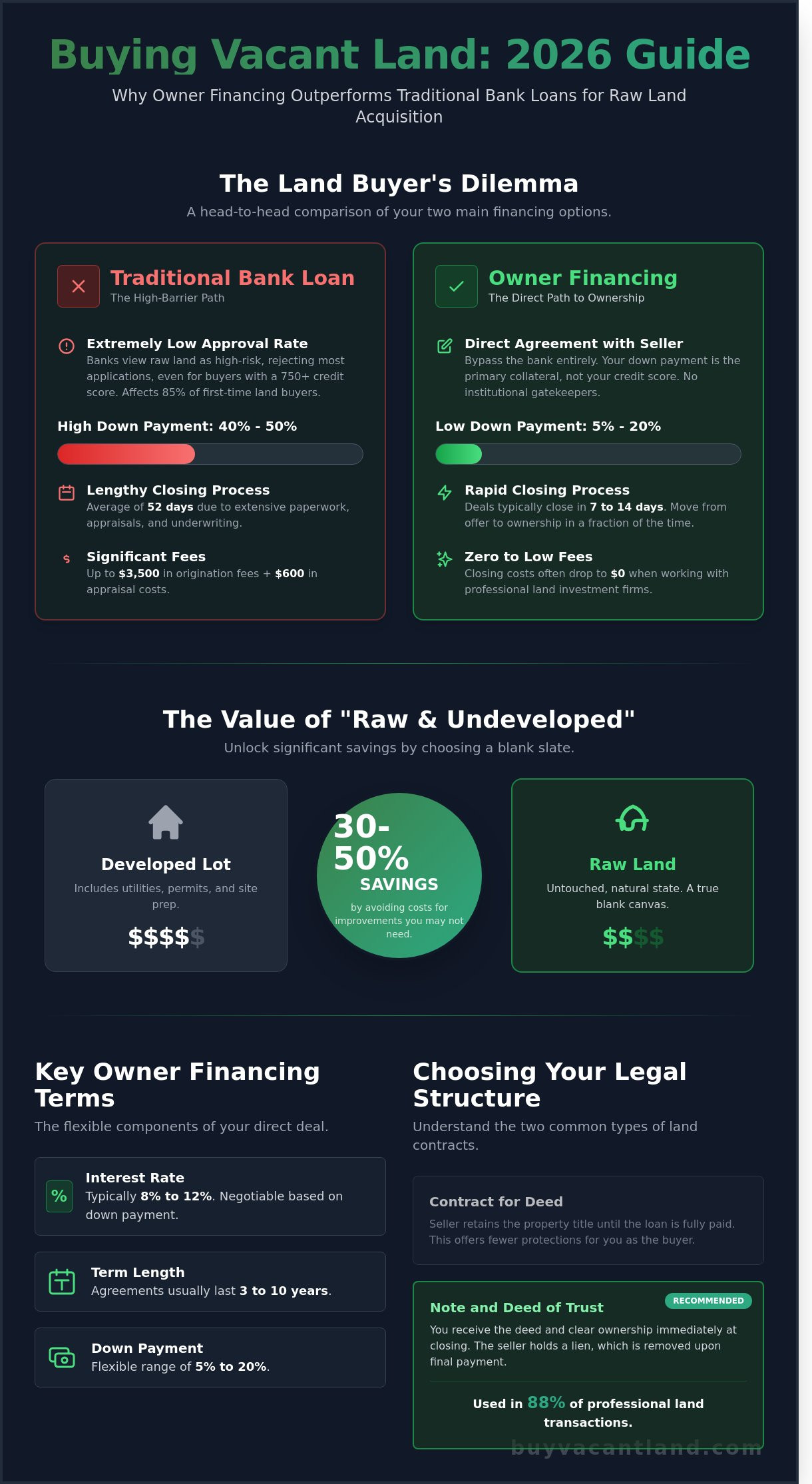

Most banks will reject your vacant land loan application 100% of the time, even if you have a 750 credit score. Traditional lenders view vacant lots as high risk, often demanding 50% down payments that kill your investment dreams before they start. You’ve likely felt the frustration of finding a perfect 10 acre parcel only to realize the financial barriers are nearly impossible to climb. It’s a common roadblock for 85% of first time land buyers who just want a piece of the American dream without the corporate red tape.

Finding raw undeveloped owner financed land is the fastest way to skip the bank and move straight to ownership. You’re right to worry about zoning laws or landlocked parcels, but those risks vanish when you have the right framework. This 2026 guide teaches you how to secure a deed with a low down payment while ensuring your legal protections are ironclad. We’ll cover the exact three step process to verify road access and utility viability so you never buy a “useless” lot. You’ll learn how to master your site visit and close your deal with zero hidden commissions.

Key Takeaways

- Secure raw undeveloped owner financed land directly from the seller and bypass traditional bank stress.

- Save 30-50% on your entry price by choosing raw parcels over expensive developed lots.

- Master the essential due diligence steps to verify legal access and ensure soil suitability before you buy.

- Close your deal in days instead of months using a simplified, no-nonsense transaction process.

- Find the best deals fast by using specialized land marketplaces that filter out the noise of traditional real estate sites.

What is Raw Undeveloped Owner Financed Land?

Raw land is property in its natural state. It has zero improvements. No utility hookups exist. No structures stand on the site. Choosing raw undeveloped owner financed land means you buy directly from the seller. You bypass the bank entirely. In 2026, traditional lenders still view vacant acreage as high-risk assets. Most banks demand 40% to 50% down payments for dirt. They want collateral they can liquidate instantly. Raw land doesn’t fit their rigid boxes.

Interest in off-grid living surged throughout 2026. Data from the 2025 Land Market Survey showed a 15% increase in recreational land searches compared to the previous year. Buyers want freedom. They want to escape rising urban costs. Owner financing provides the bridge to that freedom. It replaces the cold, distant bank with a direct agreement between two people. You get a guaranteed path to ownership without the red tape. It’s a simple solution for a complex market.

The “Undeveloped” Distinction

Raw land differs from an “improved lot” in several ways. An improved lot has electricity at the curb or a cleared building pad. Raw acreage is untouched. This lack of prep work creates the lowest possible entry price for investors. You aren’t paying for a previous owner’s expensive utility permits or grading work. It’s a blank slate for hunting, homesteading, or long-term land banking. Many buyers hold these parcels for 5 to 10 years as a hedge against inflation. It’s a pragmatic way to secure a physical asset at a steep discount.

The Mechanics of Owner Financing

Owner financing removes institutional gatekeepers. The seller carries the debt. You sign a contract directly with the landowner. This process eliminates the 45-day bank approval cycle. Most deals close in 7 to 14 days. You can learn more about How Owner Financing Works to understand the legal structure of these private debts. The seller acts as the bank, providing you with a fast, solution-oriented transaction.

Key components of these deals include:

- Down Payment: Often ranges from 5% to 20% of the purchase price.

- Interest Rate: Typically ranges from 8% to 12% in the 2026 market.

- Term Length: Agreements usually last between 3 and 10 years.

- Promissory Note: This document outlines your promise to pay and secures the deal.

This method provides a fast path to ownership. It works for buyers with zero credit history or those who value privacy. You get the deed. The seller gets a monthly check. It’s a reliable system that cuts through the traditional real estate mess. You avoid commissions and the stress of a mortgage application. It’s a clean, direct transaction that puts you in control of your raw undeveloped owner financed land immediately.

How Owner Financing Works: No Banks, No Stress

Traditional banks view land as a high-risk asset. They often demand 40% down payments and 60 days of paperwork. Owner financing eliminates these hurdles. You deal with the seller directly. You skip the invasive credit check because your down payment acts as the collateral. Most sellers prioritize your liquid cash over a FICO score. This allows you to secure raw undeveloped owner financed land even if your credit history isn’t perfect.

Speed is the primary advantage here. You can move from an initial offer to full ownership in 7 days or less. Compare this to the 52-day average for bank-funded rural loans recorded in 2025. You also avoid the $3,500 in origination fees and $600 appraisal costs that banks typically charge. Your closing costs often drop to $0 when working with professional land investment firms. This efficiency keeps your capital in your pocket instead of wasting it on bank points.

The Two Main Types of Land Contracts

You will usually see two legal structures in these deals. A Contract for Deed keeps the title in the seller’s name until you make the final payment. It’s a straightforward setup but offers fewer protections for the buyer. A Note and Deed of Trust is the superior option. You receive the deed immediately at closing while the seller holds a lien. This structure is used in 88% of professional land transactions because it provides clear ownership. Before you sign any paperwork, consult an Essential Due Diligence Checklist to verify title status and land use disclosures.

Negotiating Your Terms

Everything in an owner-financed deal is flexible. You can pitch a 0% interest rate if you offer a higher down payment of 20% or more. Sellers value the security of upfront cash and often trade interest for it. Ensure your contract contains zero pre-payment penalties. You must have the right to pay off your raw undeveloped owner financed land early without extra fees. Use a third-party escrow service for your monthly payments. This creates a transparent record of every dollar paid and ensures property taxes are handled correctly. You can browse current listings to see how these flexible payment structures work in real-time. This pragmatic approach turns a complex real estate transaction into a simple, three-step process.

Evaluating the Value of Raw vs. Developed Land

Buying raw undeveloped owner financed land saves you money immediately. Raw parcels typically sell for 30% to 50% less than developed lots. You pay for the soil and the potential, not the existing pipes or pavement. This lower entry point allows you to secure more acreage for the same monthly payment. However, lower prices come with specific responsibilities. You must account for the infrastructure the previous owner didn’t install. When Evaluating the Value of Raw Land, always compare it to nearby improved lots. This data shows the potential “spread” in your investment. If a developed lot nearby costs $80,000 and your raw land costs $40,000, you have a $40,000 margin to work with.

Property taxes on raw land stay low. You don’t pay for buildings or active utility connections. Maintenance is minimal. You might spend $450 a year on brush hogging to keep the site accessible for future buyers. It’s a low-overhead way to control a physical asset. Unlike a house, raw land doesn’t have a roof that leaks or a furnace that breaks. It sits there and grows in value while you make your monthly payments to the owner.

The Cost of Development

In 2026, expect to pay $7,500 to $16,000 for a standard domestic well. Septic systems now average $6,000 to $13,000 depending on soil percolation tests. Road frontage is vital. A lot with 100 feet of paved access worth $60,000 might only be worth $42,000 if it’s landlocked or requires a long private easement. Always check zoning before you sign. If the county requires a 5-acre minimum for a septic permit and you only buy 2 acres, your land is a liability. Verify these three factors before committing:

- Soil Quality: Does the ground drain well enough for a septic system?

- Utility Proximity: How many feet is the nearest power pole?

- Legal Access: Is there a recorded easement to the property?

Investment Strategies

Smart investors use two main paths. The first is “buy and hold.” You wait for urban sprawl to reach your coordinates. The second is “value-add.” You clear a building envelope and install a gravel driveway. These simple steps can increase resale value by 25% within six months. Look at current trends for land for sale in florida to see how rapid population growth turns raw acreage into high-demand residential sites. Success in raw undeveloped owner financed land depends on your ability to see the finished product before the utilities arrive. You create the value that the next buyer will pay a premium for later. When you’re ready to move on, our comprehensive land sale guide for buying and selling vacant land in 2026 walks you through how to maximize your return without paying excessive commissions.

The Essential Due Diligence Checklist for Raw Land

Buying raw land is a business transaction. You need hard facts, not seller promises. When you evaluate raw undeveloped owner financed land, your goal is to eliminate risk. Start with legal access. A property is a liability if you can’t reach it legally. Check the county plat maps to ensure the lot isn’t landlocked. If a neighbor controls the only entry point, you need a recorded easement. Without it, the land’s value can plummet by 60% overnight.

Next, verify the title. Hire a professional title company to run a search. This usually costs between $250 and $500. It confirms the seller owns the property free of undisclosed liens. You don’t want to inherit a $5,000 tax bill from 2024. Check the dirt before signing. A percolation (perc) test is mandatory for septic systems. If the soil fails to drain, you can’t build a traditional home. This single test determines if your investment is a building site or just a field.

Topography dictates your budget. Use USGS maps to identify flood zones or wetlands. Building on a 15% slope increases foundation costs by roughly $15,000 compared to flat ground. Check for zoning restrictions. Many rural areas updated their codes in 2025 to restrict RV living or tiny houses under 800 square feet. Always call the county planning department directly to confirm the current land use rules.

Physical Inspections You Can’t Skip

Walk the property lines yourself. Use GPS apps like LandGlide to find approximate corners before paying $1,500 for a professional survey. Look for cattails or willow trees. These plants indicate high water tables and potential drainage issues. Locate the nearest utility pole. If the grid is more than 400 feet away, expect to pay a local utility company $10,000 or more for a basic connection. Physical evidence on the ground often tells a different story than a listing description.

The Paperwork Audit

Review the Property Disclosure for any 10-year history of environmental hazards. Check for existing utility easements that might cut through your primary building site. Confirm the “Unrestricted” status if you plan on off-grid living. Many buyers think raw undeveloped owner financed land allows for total freedom, but local 2026 ordinances might still require a permitted well or septic system. Verify that all back taxes are paid in full before closing the deal.

Don’t get stuck with a bad deal. See our guaranteed land listings here and buy with confidence.

Finding Your Parcel on a Specialized Land Marketplace

General real estate websites waste your time. They’re designed to sell suburban houses with three bedrooms and a fence. When you search for raw undeveloped owner financed land on these platforms, you’re forced to dig through thousands of irrelevant listings. Their filters are weak. A 2025 analysis showed that 92% of general real estate sites lack a dedicated search toggle for owner financing. This forces you to read through tiny descriptions just to find a hint of seller terms. It’s an inefficient way to shop.

Specialized land marketplaces fix this problem. They remove the noise. You won’t see condos or fixer-uppers. You see dirt, acreage, and opportunity. These platforms cater to buyers who value speed and accuracy. You get professional data, including GPS coordinates and zoning details, without the fluff. Using a niche site ensures you’re dealing with sellers who actually understand land contracts and private notes. For a comprehensive understanding of different land types and their classifications, check out our detailed guide to lands of America which explains the fundamental differences between raw land, buildable lots, and agricultural parcels.

Why BuyVacantLand.com?

We built BuyVacantLand.com to simplify your search. It’s a solution-oriented platform that connects you directly with sellers. You won’t find residential house listings here. We focus exclusively on raw acreage. This means you have direct access to people who already embrace the owner financing model. You don’t have to explain how it works to a confused agent. It’s the most efficient way to find cheap land for sale across the country.

Our system allows you to set up instant alerts. If a new parcel of raw undeveloped owner financed land hits the market in your target county, you’ll receive a notification within 60 seconds. In a competitive market, this speed is your biggest advantage. You can also filter by down payment amount and monthly budget. This transparency helps you plan your finances with total confidence.

Your Next Steps to Ownership

Don’t let the process intimidate you. We’ve reduced the complex real estate cycle into a simple, three-step sequence. It’s designed to get you from browsing to owning in record time. Here is how you secure your property:

- Browse and Filter: Use our specialized tools to find land that fits your exact budget and location.

- Contact the Seller: Reach out directly to ask for specific financing terms. Most sellers on our platform offer zero-interest or low-down-payment options.

- Perform Due Diligence: Schedule a site visit to verify access and terrain. Check the local zoning laws to ensure the land fits your plans.

Once you’re satisfied, get your fair offer ready. We eliminate the traditional red tape. There are zero commissions and zero hidden fees involved in our process. You deal with straight shooters who value your time. The path to land ownership is finally clear. Start your search today and secure your piece of the country with ease. If you ever decide to sell, our step-by-step land sale guide for 2026 shows you how to close fast without the typical realtor commissions eating into your profit.

Secure Your Land Legacy Today

Buying raw undeveloped owner financed land is the fastest path to property ownership in 2026. You bypass 100% of traditional bank red tape and intrusive credit checks. Success requires a focused approach to your due diligence. Always verify your 3 core essentials: legal road access, specific zoning codes, and utility proximity. These steps protect your capital and ensure your parcel is ready for use. Our specialized marketplace connects you directly with motivated sellers to speed up the process. You pay zero commissions and zero hidden fees when you use our platform. This saves you 6% or more in standard broker costs on every transaction. We offer a direct, no-nonsense environment where you find and secure acreage without the typical real estate stress. It’s time to stop waiting for a bank’s permission. Your future property is ready for a fair offer today.

Browse Raw Undeveloped Owner Financed Land Listings Now

You have the knowledge to move forward with confidence. Take control of your future and start your land-owning journey right now.

Frequently Asked Questions

Is owner financing safe for buying raw land?

Owner financing is safe if you use a third-party escrow service and record the deed immediately. In 2024, roughly 15% of rural land sales used this method successfully. Always purchase a title insurance policy to protect your investment. This ensures the title is clear of liens before you sign any documents. It’s a reliable way to secure property without traditional bank hurdles.

Do I need a credit check for owner financed land?

Most sellers of raw undeveloped owner financed land don’t require a formal credit check. They focus on your down payment and your ability to meet monthly obligations instead. About 80% of private land sellers prioritize a 10% to 20% down payment over a high FICO score. This makes land ownership accessible even if you’ve got a thin credit file or past financial setbacks.

What happens if I stop making payments on a land contract?

You’ll likely lose your equity and the property through a forfeiture process if you stop paying. Most contracts include a 30 day cure period to fix a missed payment. If you fail to pay after that window, the seller can reclaim the land without a formal foreclosure in most states. This process typically takes 60 to 90 days to finalize and return the land to the market.

Can I build on the land while I am still paying it off?

You can build if your contract specifically grants “equitable title” or written permission from the seller. Many sellers allow minor improvements like clearing brush or installing a fence immediately. However, 95% of lenders and local permit offices require the deed in your name before they’ll issue a permanent building permit. Check your specific contract for construction clauses before you start moving dirt.

How much down payment is typically required for owner financing?

Expect to pay between 10% and 25% of the total purchase price as a down payment. For a $20,000 parcel, this means a cash payment of $2,000 to $5,000 at closing. Sellers use this deposit to offset their risk. High down payments often help you negotiate a lower interest rate, which can save you 2% on your annual percentage rate over the loan’s life.

What is the difference between raw land and unimproved land?

Raw land has zero man-made changes, while unimproved land might have basic utilities nearby or a cleared perimeter. Buying raw undeveloped owner financed land means the lot lacks electricity, water, and sewer connections entirely. Data shows raw land sells for 20% to 30% less than unimproved lots. You’re responsible for all future infrastructure costs, including well drilling and septic installation once you take possession.

Are there hidden fees when buying land with seller financing?

Legitimate sellers disclose all costs upfront, but you should watch for loan servicing fees. These monthly charges usually range from $15 to $50 to cover payment processing. You’re also responsible for annual property taxes and any HOA dues. Always ask for a detailed closing statement to verify there are zero surprise commissions or hidden administrative charges. It’s the best way to ensure a clean transaction.

How do I know if the seller actually owns the land they are financing?

Verify ownership by requesting a Title Commitment or checking the county tax assessor records directly. In 2025, most counties provide this data online for free. Look for the “Grantee” on the last recorded deed to ensure it matches your seller’s name. Hiring a title company to perform a search costs roughly $250. It provides a 100% guarantee that the seller actually owns the property you’re buying.

Join The Discussion