Selling your vacant lot in 2026 means facing a tax landscape where federal long-term rates hit 20% and the IRS no longer looks the other way on all-cash entity deals. You can’t use the $500,000 primary residence exclusion on empty land, which makes understanding capital gains on land sale essential for every seller. You want a fair return on your investment, not a headache filled with confusing terminology and hidden fees. It’s stressful to watch your hard-earned equity vanish into tax brackets you don’t fully understand.

This guide explains exactly how the tax system works so you can stop guessing and start planning. You’ll learn how to calculate your 2026 liability using the latest federal rates and discover legal strategies like 1031 exchanges or installment sales to lower your bill. We’ll show you which expenses are deductible and provide a simple path to selling your land fast for cash. From new FinCEN reporting rules to state-specific tax traps, you’ll get the facts you need to close your deal with confidence and keep more of your proceeds.

Key Takeaways

- Identify why the IRS treats vacant land differently than residential property and how this impacts your total tax bill.

- Learn how to use your adjusted cost basis to legally reduce your taxable profit and minimize the capital gains on land sale.

- Compare federal short-term and long-term tax rates to determine the most profitable time to list your property.

- Explore five proven methods, such as 1031 exchanges and installment sales, to defer taxes and keep more of your cash.

- Organize a “Basis Folder” with specific deductible expenses to prove your numbers and ensure a fast, hassle-free exit.

Understanding Capital Gains Tax on Land Sales in 2026

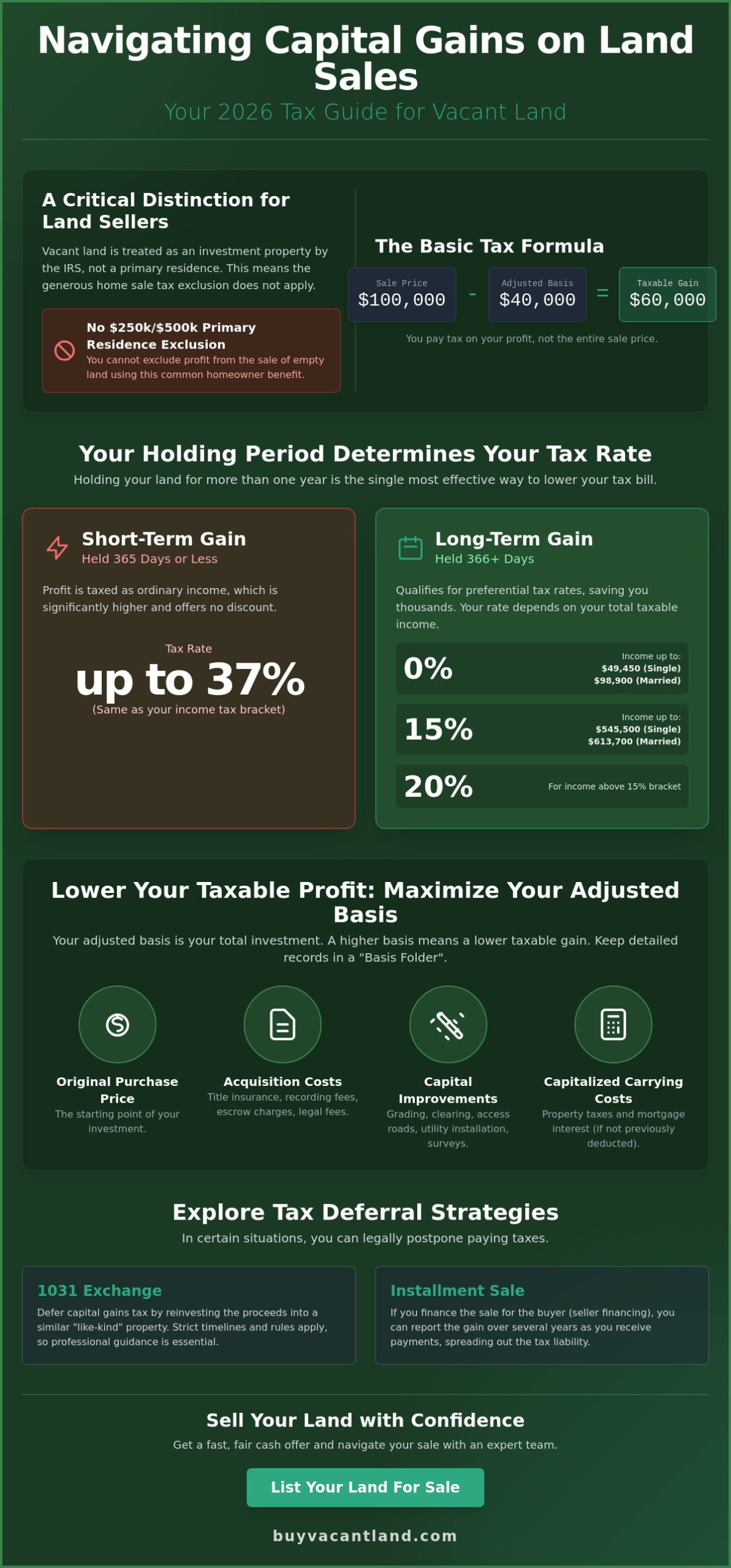

Understanding What is a capital gain? is the first step toward a successful land sale. In simple terms, it’s the tax you pay on the profit earned from selling an asset. When you sell vacant land, the IRS views the transaction as a realization of investment growth. The 2026 tax environment is strict, and the IRS has increased its focus on real estate transparency. You need to know the rules to keep more of your cash and avoid a surprise bill.

The math behind your tax liability is direct. The basic formula is: Sale Price – Adjusted Basis = Taxable Capital Gain. If you sold a residential lot for $100,000 and your basis was $40,000, you owe taxes on the $60,000 difference. Your basis starts with what you originally paid for the land. It also includes certain closing costs and improvements. If you don’t track these numbers, you’re giving away money. It’s that simple. In 2026, market stabilization means your profit margins depend entirely on how well you manage these tax details.

Is Vacant Land Eligible for the Primary Residence Exclusion?

Most sellers assume they can use the Section 121 exclusion to avoid taxes. This is a common mistake. This exclusion usually requires a physical dwelling where you have lived for two of the last five years. If you’re selling empty land, you don’t have a home to claim. You can’t exclude $250,000 or $500,000 of profit like a traditional homeowner. There is a rare exception if the land is adjacent to your primary home and you sell both as part of the same transaction. For most sellers of off-grid land or farms, you should plan for a capital gains on land sale tax bill from day one.

The Difference Between Short-Term and Long-Term Gains

The IRS rewards patience. Timing is the biggest factor in how much cash you keep. If you sell your land within 365 days of buying it, the profit is a short-term gain. This is expensive. Short-term gains are taxed at your ordinary income rate, which can reach 37% in 2026. Hold that land for 366 days or more to trigger long-term rates. These preferential rates are significantly lower:

- 0% Rate: Applies if your taxable income is below $49,450 (single) or $98,900 (married filing jointly).

- 15% Rate: Applies to most sellers with income up to $545,500 (single) or $613,700 (joint).

- 20% Rate: Applies to high earners exceeding those thresholds.

Moving from a short-term to a long-term hold can save you thousands of dollars in guaranteed profit. Check your deed date before you sign a contract. A few extra days of ownership could be the difference between a massive tax bill and a tax-free exit.

Calculating Your Profit: Maximizing the Adjusted Cost Basis

Your adjusted cost basis is the most important number in your transaction. It represents your total investment in the property. A higher basis means a lower taxable profit. This directly reduces the capital gains on land sale you’ll report to the IRS. Don’t just look at the original sticker price. You must include every dollar you spent to acquire and hold the property. If you ignore these costs, you’re essentially volunteering to pay more tax than you owe.

Start with the purchase price. In Q1 2026, the median price per acre for land listings hit $62,365. If you bought your parcel years ago for a fraction of that, your profit margin is likely high. You can offset this gain by adding original closing costs. Title insurance, recording fees, and escrow charges are all part of your basis. The IRS rules on capital gains allow these additions because they’re acquisition costs. Every dollar added to the basis is a dollar that isn’t taxed at your 2026 rate.

Land-Specific Expenses That Increase Your Basis

Raw land requires work to become valuable. These costs aren’t repairs; they’re capital improvements. If you cleared heavy brush, graded the soil, or cut in an access road, add those invoices to your basis. Legal fees for zoning changes or title clearing also count. Bringing utilities like water or power to the lot line is another major addition. These expenses permanently increase the land’s value. Keep every receipt. If you can’t prove the expense, you can’t deduct it. If you’re looking for a quick exit after these improvements, you can list your land for sale on our specialized marketplace to find cash buyers fast.

Carrying Costs: Can You Deduct Property Taxes and Interest?

Many land owners ignore carrying costs. This is a mistake. If you didn’t deduct property taxes or mortgage interest on your annual tax returns, you can capitalize them. This means you add them to your basis instead of taking a yearly deduction. This strategy is vital for undeveloped land that doesn’t produce income. It turns years of holding costs into a tax-saving shield at the time of sale. You need precise records for every year of ownership to make this work. Tracking these costs over a decade can erase thousands from your taxable gain. It’s a pragmatic way to protect your proceeds without using complex loopholes.

Short-Term vs. Long-Term Capital Gains: A 2026 Comparison

Your holding period determines your final tax rate. If you sell your land within 365 days of buying it, the IRS classifies the profit as a short-term gain. This is a costly move. Short-term gains are taxed as ordinary income. Depending on your total earnings, you could pay up to 37% in federal taxes. Waiting until day 366 changes the rules in your favor. Long-term 2026 capital gains tax rates are significantly lower. Selling at 11 months is a major financial mistake. You’re essentially handing over a massive portion of your profit just to close a few weeks early. Patience puts more cash in your pocket.

The 2026 tax brackets are designed to reward long-term investors. For most sellers, the difference between short-term and long-term rates is at least 10% to 20%. If you’re selling a high-value parcel, that percentage represents thousands of dollars. Your total annual income from all sources dictates which bracket you fall into. A successful land sale increases your taxable income, which can shift your tax strategy. You must look at your entire financial picture before you agree to a closing date. Timing is the most effective tool you have to control your capital gains on land sale liability.

The 15% Sweet Spot for Most Land Sellers

Most land sellers aim for the 15% long-term bracket. In 2026, this bracket applies to single filers with taxable income between $49,451 and $545,500. For married couples filing jointly, the range is $98,901 to $613,700. If your total income stays within these bounds, you’ll pay 15% on your land profit. Be careful with large transactions. A significant gain can “push” your total income into the 20% bracket. Strategy matters here. You might choose to sell in a year when your other income is lower to stay in a more favorable bracket and maximize your proceeds.

Net Investment Income Tax (NIIT) for High Earners

High earners must plan for an extra cost. The Net Investment Income Tax (NIIT) is an additional tax on investment income above specific thresholds. This 3.8% tax triggers when your Modified Adjusted Gross Income (MAGI) exceeds $200,000 for single filers or $250,000 for married couples. If you hit these limits, your capital gains on land sale will be taxed at your long-term rate plus the 3.8% surcharge. This tax is not indexed for inflation, so it affects more sellers every year. Calculate your projected MAGI early to see if this extra bill will impact your final payout.

5 Proven Strategies to Reduce or Defer Your Land Sale Taxes

You don’t have to accept a massive tax bill as an unavoidable cost of doing business. Several legal paths allow you to keep more of your money after a sale. These strategies focus on timing, reinvestment, and income management. When you receive a fair cash offer for your property, your goal is to protect as much of that equity as possible. In the 2026 market, where land prices have stabilized after years of rapid growth, protecting your margins is more important than ever. Use these IRS-approved methods to lower your capital gains on land sale liability.

One of the most effective ways to lower your bill is through tax loss harvesting. You can use capital losses from other investments to offset your land profits. If you sold stocks or other real estate at a loss earlier this year, those losses cancel out your gains dollar-for-dollar. There’s no limit on using capital losses to offset capital gains. It’s a direct, pragmatic way to balance your portfolio. If you want to see what your property is worth before choosing a strategy, you can get your fair cash offer today and start planning your exit.

The 1031 Exchange for Vacant Land

The 1031 exchange is the gold standard for tax deferral. It allows you to swap your land for another “like-kind” investment property without paying immediate taxes. The definition of like-kind is broad. You can trade raw land for an apartment building, a commercial lot, or another parcel of undeveloped acreage. You must follow strict timelines to qualify. You have exactly 45 days after your sale to identify a replacement property. You must close on that new property within 180 days. You cannot touch the sale proceeds during this time. A Qualified Intermediary (QI) must hold the cash in escrow to keep the exchange valid.

Using Installment Sales to Lower Your Bracket

An installment sale spreads your profit over several years. This is exactly how owner financed land works as a tax-saving tool. Instead of taking a lump sum and hitting a high tax bracket, you receive payments over time. You only pay capital gains on land sale on the portion of the principal you receive each tax year. This strategy can keep your total annual income low enough to stay in the 15% or even the 0% long-term bracket. It turns a one-time tax hit into a manageable, long-term income stream. You avoid the “bracket creep” that often happens with large, single-year real estate transactions.

Navigating the Sale: Preparing Your Land for a Tax-Efficient Exit

Finalize your exit strategy now. You need a “Basis Folder” to survive an IRS audit. This folder should hold every receipt, invoice, and closing statement from your ownership period. Without these documents, you can’t prove your deductions. You’ll end up paying capital gains on land sale on money you didn’t actually profit. Preparation creates speed. Speed creates peace of mind. Before you sell land, ensure your records are bulletproof.

Get a professional valuation. National land prices per acre hit a median of $62,365 in Q1 2026. Don’t guess your price. An accurate valuation ensures you don’t leave cash on the table. It also prevents your property from sitting stagnant while inventory levels fluctuate. Land inventory contracted by 23.6% between 2019 and early 2026, meaning serious buyers are actively hunting for deals. Specialized marketplaces connect you with these buyers fast. This is how you move property without the typical residential red tape.

Zero Commission: The BuyVacantLand.com Advantage

Agents often take 6% to 10% in commissions on land sales. That’s a massive hit to your equity. It makes your tax burden feel even heavier because you’re losing money before the IRS even takes its cut. A direct listing on BuyVacantLand.com removes that middleman. You save thousands of dollars instantly. Our three-step process is simple. You list your parcel, connect with buyers, and close the deal. No hidden fees. Zero commissions. Just a straight path to your cash.

Consulting a Tax Professional

Large land sales warrant a professional CPA review. Tax laws are complex and change quickly. A single mistake can trigger an audit or a higher capital gains on land sale rate. Ask your advisor about state-specific exclusions or the 2026 FinCEN reporting rules for all-cash deals made through LLCs. Get your answers before you sign the closing docs. Once the deal is done, the tax liability is locked in. List your land today and move toward your next investment with confidence.

Take Control of Your 2026 Land Sale Today

Managing your capital gains on land sale doesn’t have to be a burden. You now have the tools to lower your tax liability legally. Focus on maximizing your adjusted cost basis by tracking every improvement and carrying cost. Remember that holding your property for at least 366 days triggers preferential long-term rates that protect your equity. These simple steps ensure you keep more cash in your pocket when it’s time to close the deal.

Don’t let traditional real estate fees eat into your hard-earned profit. Our specialized marketplace connects you directly with thousands of cash buyers across the country. We charge zero commissions and no hidden fees. This direct approach simplifies the process and maximizes your final payout. You can list your vacant land for sale today and keep more of your profit. It’s the fastest way to turn your unwanted parcel into a guaranteed cash return. Take the first step toward a stress-free transaction and start your listing now.

Frequently Asked Questions

How is capital gains tax calculated on land?

You calculate your tax by subtracting your adjusted cost basis from the final sale price. Your basis includes the original purchase price plus closing costs and capital improvements like clearing or road construction. The resulting number is your taxable profit. If you held the land for more than a year, you apply long-term rates to this amount. If you held it for a year or less, it’s taxed as ordinary income. Accuracy in these calculations ensures you don’t overpay the IRS.

Can I avoid capital gains tax by buying another piece of land?

Yes, you can defer taxes by using a 1031 Exchange to reinvest your proceeds into a like-kind property. This process allows you to swap one investment parcel for another without triggering an immediate tax bill. You must use a Qualified Intermediary to hold the funds and follow strict federal timelines. This strategy is a powerful way to grow your portfolio while keeping your equity intact. It turns a potential tax hit into a tool for future wealth building.

What is the long-term capital gains rate for 2026?

The federal long-term capital gains on land sale rates for 2026 are 0%, 15%, or 20%. Most individual sellers fall into the 15% bracket if their taxable income is between $49,451 and $545,500. Married couples filing jointly stay in the 15% bracket up to $613,700 in income. High earners exceeding these amounts pay the 20% rate. These rates only apply to land held for at least 366 days. Timing your sale to fit these brackets can save you thousands in taxes.

Is there a difference in tax between selling raw land and a farm?

The IRS generally treats both raw land and farms as investment assets, but farms involve more complexity. If your farm includes structures or equipment you depreciated, you may face depreciation recapture taxes. This portion of your gain is often taxed at a higher rate of up to 25%. Raw land is simpler because it doesn’t involve depreciation. Both property types qualify for 1031 exchanges. Always check your depreciation records before selling agricultural property to avoid surprise liabilities.

Can I deduct the cost of a survey from my capital gains?

Yes, you can add the cost of a professional survey to your adjusted cost basis. A survey is considered a capital improvement or an acquisition cost that increases the value of your property. By increasing your basis, you legally lower your taxable profit. This directly reduces the total capital gains on land sale you owe. Keep your survey invoice in your permanent records. It’s a pragmatic way to protect your proceeds and prove your investment to the IRS.

How long do I have to reinvest land sale proceeds to avoid taxes?

You have exactly 180 days to complete a 1031 Exchange and avoid immediate taxation. This clock starts the day you close the sale of your original property. You must also identify your replacement property in writing within the first 45 days of that period. These deadlines are rigid and have no extensions. If you miss a single day, the IRS will tax the entire gain. Proper planning with a professional intermediary is essential to meet these requirements.

What happens if I sell my land for a loss?

Selling at a loss creates a capital loss that you can use to offset other capital gains. If your total losses exceed your gains, you can use up to $3,000 of the excess to offset your ordinary income. Any remaining loss carries forward to future tax years. This “tax loss harvesting” is a smart way to balance your investment portfolio. It turns a disappointing sale into a strategic tax shield. You can’t claim a loss on land held strictly for personal use, such as a backyard extension.

Does the IRS consider vacant land an investment or personal property?

The IRS usually classifies vacant land as an investment asset unless you specifically hold it for personal enjoyment. If you bought the land with the intent to sell it for profit, it’s an investment. This classification is beneficial because it allows you to deduct capital losses. Personal use property, like a lot used only for family camping, doesn’t allow for loss deductions. Most raw land sellers fall into the investment category. This status provides more flexibility for using basis adjustments and tax deferral strategies.

Join The Discussion