Why let a bank’s rigid lending requirements stand between you and your future property? For many, the dream of owning a residential lot or off-grid acreage dies at the loan officer’s desk. Understanding a land contract is the fastest way to bypass the 20% to 50% down payments banks often demand for raw, undeveloped land. You already know that traditional financing is slow, expensive, and filled with unnecessary hurdles. The high closing costs and strict credit checks make simple land ownership feel impossible.

We are here to simplify the process. This guide provides a clear, pragmatic breakdown of how land contracts work so you can buy or sell vacant land without bank interference. You will get the facts on payment structures, current interest rates, and the critical difference between legal and equitable title. We lay out a direct path to land ownership that avoids the mortgage trap and eliminates common service fees. Follow this straightforward sequence to gain the confidence you need to sign your next seller-financed agreement and secure your asset today.

Key Takeaways

- Bypass bank bureaucracy by negotiating directly with the seller for a faster, simpler path to land ownership.

- Save time and money with minimal closing fees and a transaction timeline that takes days instead of months.

- Gain a clear advantage by understanding a land contract’s payment structures and negotiation points to secure property without a mortgage.

- Protect your investment by identifying essential legal clauses, such as title verification and the “Right to Cure.”

- Streamline your search by using specialized marketplaces to find residential lots and off-grid land with owner financing already available.

What is a Land Contract for Vacant Land?

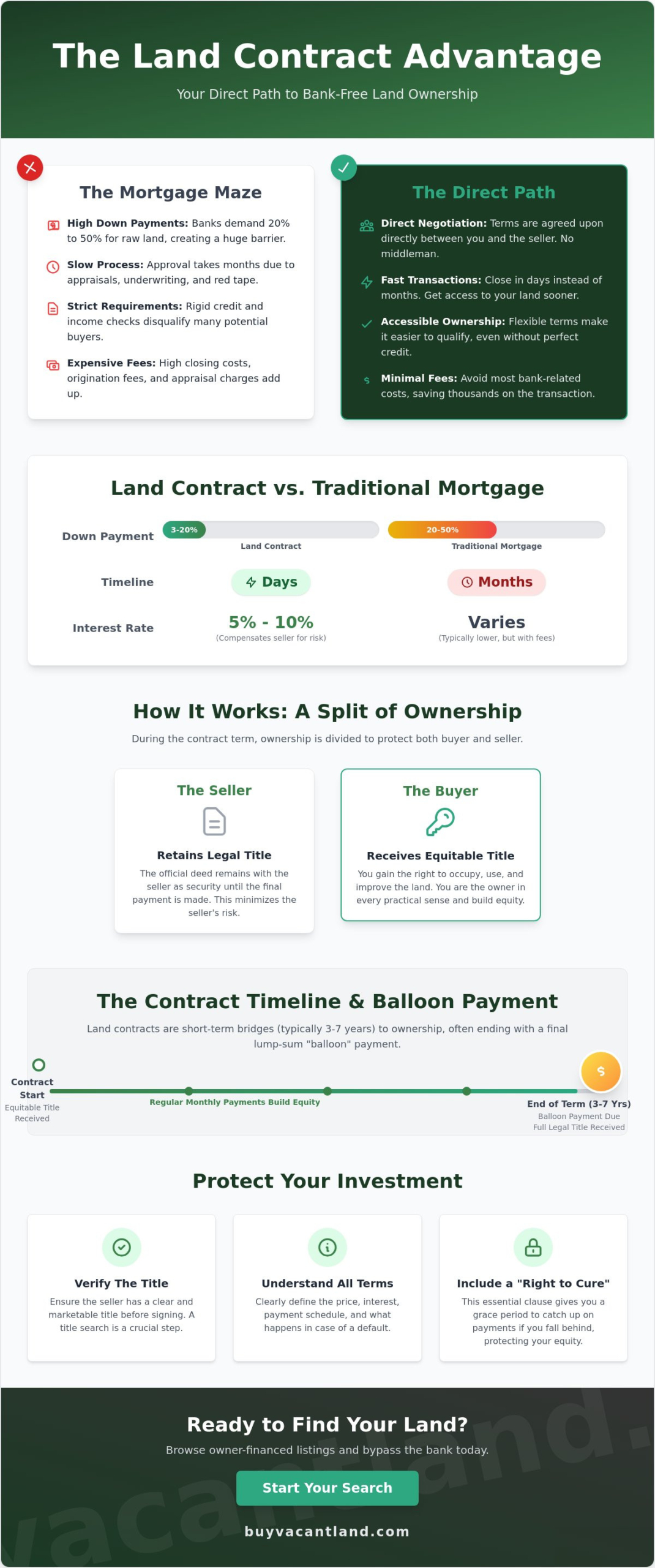

A Land contract is a direct, seller-financed agreement for purchasing property. It eliminates the middleman. Instead of begging a bank for a mortgage, you negotiate terms directly with the person who owns the dirt. Understanding a land contract is vital because it changes the fundamental rules of real estate acquisition. You make your monthly payments to the seller. They act as the lender. This arrangement is the primary way to secure owner financed land in the United States. It is a streamlined path to ownership that prioritizes speed and direct communication over bureaucratic delays.

In this setup, the transaction remains private. There are no loan origination fees, no expensive bank appraisals, and no lengthy underwriting processes. You and the seller agree on the price, the down payment, and the monthly installment. Once both parties sign, you have a binding agreement that bypasses the traditional financial system entirely. It is a pragmatic solution for people who want to own property without the stress of institutional oversight.

The Core Concept: Legal vs. Equitable Title

Ownership is split into two distinct parts during the life of the agreement. The seller retains the legal title. This acts as security for the debt. If you stop paying, they still hold the deed. You receive equitable title the moment the contract is signed. This grants you the right to occupy the land, build on it, and maintain it. You are the owner in every practical sense. You gain the right to build equity and benefit from any appreciation in the land’s value. You receive the full legal deed only after you satisfy the final payment. It is a clean, performance-based swap.

Why Land Contracts are Essential for Raw Land

Traditional lenders are notoriously difficult when it comes to undeveloped land. They view raw acreage as a high-risk asset because there is no structure to serve as collateral. Most big banks demand massive down payments, sometimes as high as 50 percent, or they refuse to lend altogether. Understanding a land contract helps you see why this tool is a game changer for the land market.

- Speed: Sellers move inventory faster by offering flexible terms that banks won’t touch.

- Accessibility: Buyers avoid the rigid credit and income requirements of big banks.

- Efficiency: The process removes the layers of red tape that typically stall rural land deals.

This method provides a reliable problem-solving framework. It cuts through the procedural hurdles that stop most land purchases before they even start. You get the land you want. The seller gets a steady return. The bank is left out of the equation entirely.

The Mechanics: How a Land Agreement Functions

Understanding a land contract requires looking at the specific math of the deal. Unlike bank loans with rigid formulas, these agreements are highly customizable. You and the seller negotiate every detail. This includes the purchase price, the down payment, and the interest rate. Because the seller is taking on the role of the lender, they assume more risk. To compensate for this, interest rates for seller financing in 2026 typically range between 5% and 10%. While this is higher than a standard mortgage, you save thousands in bank fees and origination costs.

The down payment is often the most flexible part of the transaction. In traditional land loans, banks might demand 30% or more. With a land contract, down payments are often between 3% and 20%. This lower entry point makes it possible to secure a property that would otherwise be out of reach. However, you must be aware of the risks of land contracts if the terms are not clearly defined. A well-structured agreement protects your equity and ensures a transparent path to full ownership.

Common Payment Structures

Most agreements follow one of two paths. Amortized payments spread the principal and interest over a fixed term, such as 5 or 10 years. This allows you to build equity with every check you write. Alternatively, some sellers offer interest-only payments. This structure keeps your monthly costs low but does not reduce the principal balance. It is a pragmatic choice if you plan to develop the land quickly and refinance later. If you are ready to see what is available, you can browse owner-financed listings to compare different payment structures in real time.

The Role of the Balloon Payment

Most land contracts are not designed to last 30 years. They are short-term bridges, usually lasting between 3 and 7 years. Because the payments are often calculated as if the loan were longer, a large balance remains at the end of the term. This is the balloon payment. You must pay this lump sum to receive the final deed. Many buyers use this time to improve the land, increase its value, and then qualify for a traditional bank refinance to pay off the seller. It is an efficient way to get your foot in the door while you prepare for long-term financing.

Land Contract vs. Traditional Mortgage: A Pragmatic Comparison

Speed is the ultimate currency in real estate. Traditional mortgages are slow. They require appraisals, inspections, and weeks of underwriting. A land contract cuts the timeline from months to days. You bypass the 2% to 6% closing cost burden typically associated with bank-originated loans. Understanding a land contract means recognizing that you are trading bank-mandated bureaucracy for immediate access and lower upfront fees. It is a direct solution for those who value time and efficiency.

Credit requirements also differ wildly. Banks rely on a rigid FICO score. If your score is low, the door is closed. Sellers use their own discretion. They look at your down payment and your ability to pay. This creates a path to ownership for those the traditional system ignores. However, sellers maintain more control. If a buyer defaults, the legal process is often faster and less complex because the seller already holds the legal title. It is a performance-based agreement that rewards consistency.

Pros and Cons for the Land Buyer

Pros include easier qualification and nearly instant access to the property. You don’t wait for a loan officer’s approval to start using your land. On the downside, you must watch for “due on sale” clauses. If the seller has an existing mortgage, the bank could demand full payment if they discover the contract. Additionally, you are responsible for property taxes and insurance immediately. Budget for these costs from day one to avoid surprises.

Pros and Cons for the Land Seller

Sellers benefit by moving inventory at a higher price point while earning 5% to 10% interest. It turns a stagnant asset into a stream of passive income. Retaining the legal title provides a powerful safety net. If the buyer stops paying, you keep the land and the payments made. The primary risk is the condition of the land. A defaulting buyer might leave behind debris or environmental issues that you must resolve. Screen your buyers carefully to ensure a smooth transaction.

Essential Clauses and Red Flags to Watch For

Precision in your paperwork prevents future disasters. Understanding a land contract requires a deep dive into the fine print before you sign anything. Your first priority is verifying ownership. Never take a seller’s word for it. Conduct a professional title search to ensure the property is free of undisclosed liens, judgments, or back taxes. If the seller doesn’t own the land free and clear, your investment is at risk from their creditors. This simple step establishes a foundation of certainty for the entire transaction.

A “Right to Cure” clause is a non-negotiable requirement for buyer protection. This provision gives you a specific grace period, typically 15 to 30 days, to catch up on a missed payment before the seller can initiate a default. Without it, a single late check could theoretically cost you the land and every dollar you’ve already paid. You must also confirm the contract is recordable at the county level. Recording the document puts the world on notice that you have a legal interest in the property. It prevents the seller from selling the land to someone else or using it as collateral for new loans. If you are ready to find secure opportunities with transparent terms, search for verified owner-financed land now.

Protecting Your Investment

Don’t skip the due diligence. Include a specific clause that allows for property inspections and environmental testing. You need to know if the soil can support a septic system or if there are hidden easements that restrict building. Ensure the contract explicitly states who is responsible for property taxes and insurance. Usually, the buyer assumes these costs immediately. Define the default process with absolute clarity. Both parties should know exactly what happens if the agreement fails. A transparent process avoids long, expensive legal battles and provides peace of mind for everyone involved.

Red Flags in Land Agreements

Watch for deal-breakers that favor the seller exclusively. Some contracts prohibit you from making any improvements to the land until the final payment is made. This is a massive red flag. it stops you from building value and preparing the land for a future refinance. Avoid extremely short balloon payment windows. A one-year or two-year term is often a trap designed to trigger a default so the seller can keep your down payment and the land. Finally, walk away if a seller refuses to provide a written, recordable agreement. A handshake deal in real estate is a recipe for total financial loss.

How to Find and Buy Owner-Financed Land Deals

Finding the right property is the final step in understanding a land contract. You must look where the banks aren’t. Most general real estate websites focus on houses and traditional mortgages. They don’t cater to the nuances of raw land. To find owner-financed deals, use specialized marketplaces like BuyVacantLand.com. These platforms allow you to filter specifically for properties where the seller is willing to act as the bank. Look for listings explicitly tagged as “Seller Financing Available” or “Land Contract.” This targeted search saves you hours of wasted time and frustration. It connects you directly with sellers who already understand the value of an equitable financial proposal.

Be proactive in your search. If you find a parcel that fits your needs but doesn’t mention financing, message the seller directly. Ask if they are open to an installment sale. Many land owners prefer the steady monthly income of a land contract over a one-time cash payment that gets hit by heavy taxes. Establishing a direct line of communication is the fastest way to negotiate favorable terms. For a broader look at the entire acquisition process, review our guide on how to buy land. It provides the general due diligence steps you need to take before signing any paperwork.

Navigating the Marketplace

Efficiency is your greatest asset. Search specifically for cheap land for sale to find motivated sellers. These owners are often more flexible with their terms to ensure a quick, clean transaction. Use the platform’s advanced filters to narrow your search by acreage, zoning, and available financing options. This prevents you from chasing deals that don’t fit your budget or your plans. Once you find a match, contact the seller immediately. Direct communication removes the layers of bureaucracy that slow down traditional sales. It builds the rapport necessary for a smooth closing.

Closing the Deal Efficiently

A successful close relies on speed and absolute clarity. Once you find the right lot and confirm the seller’s ownership, follow this streamlined sequence to completion:

- Agree on terms: Finalize the purchase price, the down payment amount, and the interest rate.

- Draft the contract: Ensure a simple, written agreement reflects every verbal promise. It must include the payment schedule and the balloon payment date.

- Notarize: Sign the document in the presence of a notary to verify all identities.

- Record the document: File the contract at the county recorder’s office. This is the hallmark of a secure deal. It protects your equitable title against any future claims.

This straightforward path eliminates the stress of bank hurdles. It provides a sense of momentum that pushes you toward the final goal of land ownership. You get the property you want without the wait. By following this simplified, numbered sequence, you can secure your asset with total confidence and zero service fees.

Secure Your Land Without the Bank

You now have the framework to bypass traditional bank bureaucracy and secure your property on your own terms. Understanding a land contract allows you to trade slow underwriting processes for a fast, direct agreement with the seller. You know how to structure payments, verify title, and identify the red flags that stall most land deals. This pragmatic approach puts you in control of your financial future and eliminates the burden of high closing costs.

Stop letting rigid lending requirements dictate your path to ownership. Take the final step by visiting a specialized marketplace built for bank-free transactions. You can Browse Owner-Financed Land Listings on BuyVacantLand.com to get direct access to thousands of vacant land parcels. There are no hidden service fees for buyers. It is the most efficient way to find residential lots, off-grid land, or acreage with an equitable financial proposal already in place.

The path to owning your own dirt is clear. Start your search today and secure your asset with total confidence.

Frequently Asked Questions

Is a land contract the same as a rent-to-own agreement?

No, they are legally distinct. In a land contract, you are purchasing the property from day one and gain equitable title. Rent-to-own is a lease where you pay rent for the right to potentially buy the property later. Understanding a land contract means recognizing that you are the owner in every practical sense, responsible for the land’s taxes and upkeep immediately.

What happens if a buyer defaults on a land contract?

The seller generally keeps the property and all previous payments if you default. Since the seller retains the legal title, they can often reclaim the land through a process called forfeiture, which is faster than a traditional bank foreclosure. This makes consistent payments critical. Always check for a “Right to Cure” clause to give yourself a grace period before losing your equity.

Can I build a house on land I am buying through a land contract?

Who pays property taxes on a land contract?

Can a seller back out of a land contract?

A seller cannot back out of a signed agreement without a specific legal reason defined in the contract. Once you sign and record the document, the seller is legally obligated to transfer the deed once you complete the payment schedule. If a seller attempts to break the deal, you have the right to seek legal enforcement of the contract terms.

How do I refinance a land contract into a traditional mortgage?

You refinance by applying for a traditional bank loan once you have enough equity or have improved the land’s value. The bank pays the seller the remaining balance in full, and you receive the legal deed. This is a common strategy for handling the final balloon payment. It effectively replaces the seller’s higher interest rate with a long-term bank mortgage.

Do land contracts require a credit check?

Credit checks are entirely up to the seller’s discretion. Most sellers care more about a substantial down payment than a perfect FICO score. This flexibility is a core benefit of understanding a land contract. It provides a path to ownership for buyers who might be rejected by traditional lenders due to strict income or credit history requirements.

Should I record my land contract with the county?

You should always record the contract at the county recorder’s office. Recording creates a public record of your interest in the land. This prevents the seller from taking out new loans against the property or selling it to another buyer. It is your primary legal defense and ensures your path to receiving the full legal title is secure and transparent.

Join The Discussion